Alternative Credit outlook : Adapting to divergence and disruption

Macro uncertainty is impacting the investment landscape

Despite the recent de-escalation in tensions between the US and China, the trade war continues to represent a significant shock to the global economic outlook. Lingering tariffs, disrupted supply chains and heightened uncertainty weigh on investment sentiment and growth. Tariffs and geopolitical uncertainties are expected to harm the global economy in both the short and medium term.

In Europe, renewed focus on defense and infrastructure aims to stimulate growth and address broader structural issues. However, persistent global economic uncertainty has led many firms to delay investments, adopting a cautious stance that is dampening overall activity and directly affecting the investment universe.

Diverging interest rate regimes

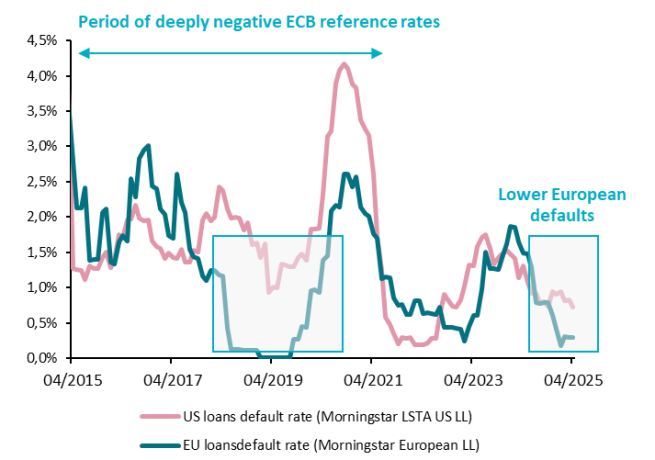

Central banks are expected to maintain their easing stance, which is broadly supportive of economic activity, real estate markets, and lowers financing costs for both businesses and households. However, a key divergence is emerging between the European Central Bank (ECB) and the US Federal Reserve (Fed).

The Fed faces constraints due to a stagnating US economy, limiting its ability to pursue aggressive easing. In contrast, the ECB has accelerated its easing in response to disinflation and weaker economic conditions. This divergence is reflected in market expectations for terminal rates, with implications for credit performance.

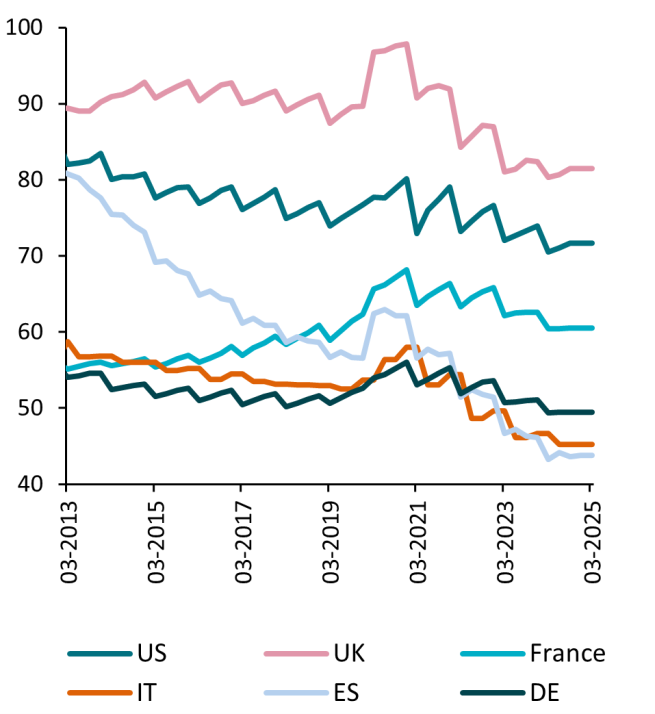

Notably, during the ECB’s negative rate period from 2015 to 2022, European corporates showed lower default rates than their US counterparts, and the same will likely play out for as long as interest rate trajectories diverge.

Continued lower rates in Europe are expected to further support corporate stability, households, and real estate. This outlook is prompting a growing number of international investors to increase their exposure to private credit opportunities in Europe.

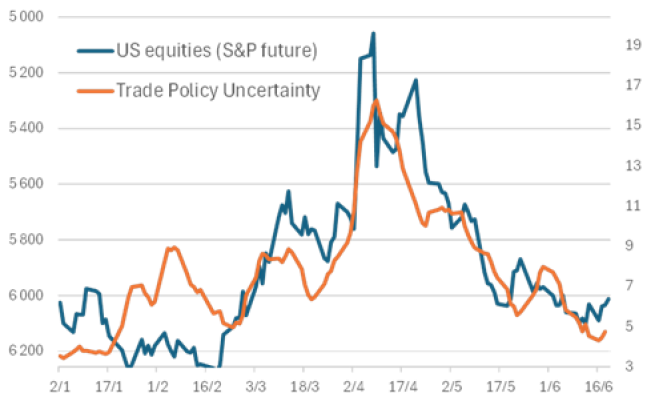

Higher market volatility creates opportunities

Recent trade wars and tariffs have increased market volatility, contributing to wider credit spreads in liquid alternative assets like loans (BSL) and alternative credit structured products (CLO/ABS). While uncertainty persists, this environment presents attractive entry points for high-quality senior assets with embedded structural protection against recession risks.

Private markets have remained relatively insulated due to their slower adjustment, typically lagging public markets by 3 - 6 months, though early signs of spread widening are emerging in our negotiations for private credit deals.

Corporate assets

Upward revision for European earnings

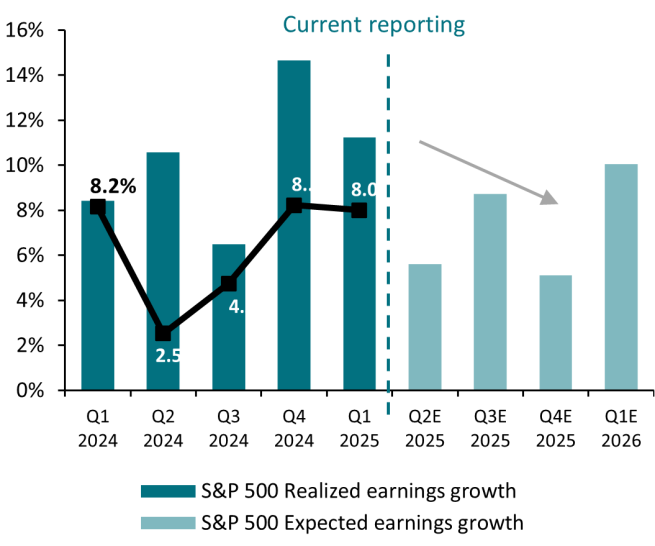

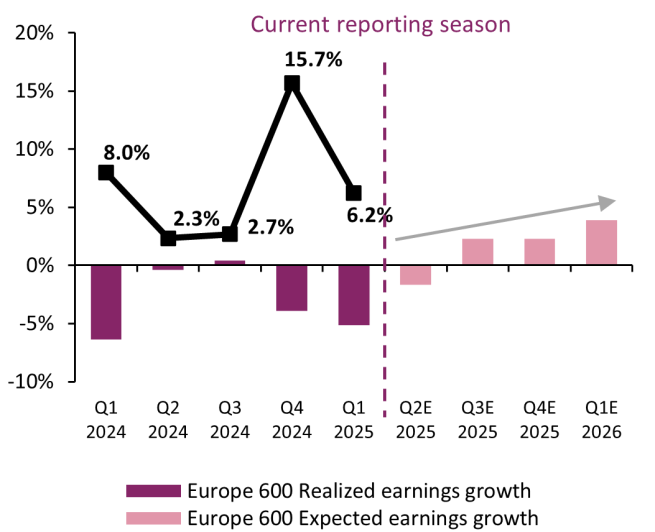

US corporate earnings for Q1 2025 exceeded expectations by around 8%[1], but tariffs have caused uncertainty, leading firms to delay future decisions and analysts to revise growth forecasts downward. In contrast, European earnings, though weaker, have surpassed expectations and improved economic sentiment in Europe has prompted analysts to raise their earnings projections.

Corporates still benefit from good access to capital

Loan issuance was strong in 2024, driven mainly by refinancing and opportunistic repricing, which made up two-thirds of activity. This trend continued in Q1, alongside a modest rise in M&A and LBO deals.

Large companies benefited from abundant liquidity amid strong competition between broadly syndicated loans (BSL) and direct lenders. The lines between private and public markets have blurred, with more direct lenders financing traditionally syndicated deals. This has helped companies extend maturities beyond 2025, pushing the main maturity wall to 2028–2032 and reducing refinancing risk.

M&A and LBO activity slower to rebound

Market volatility and swings in long-term rates may delay a full rebound in M&A and LBO activity in 2025. However, private equity firms face pressure to exit long-held investments - now averaging nearly six years - amid high rates and valuation uncertainty.

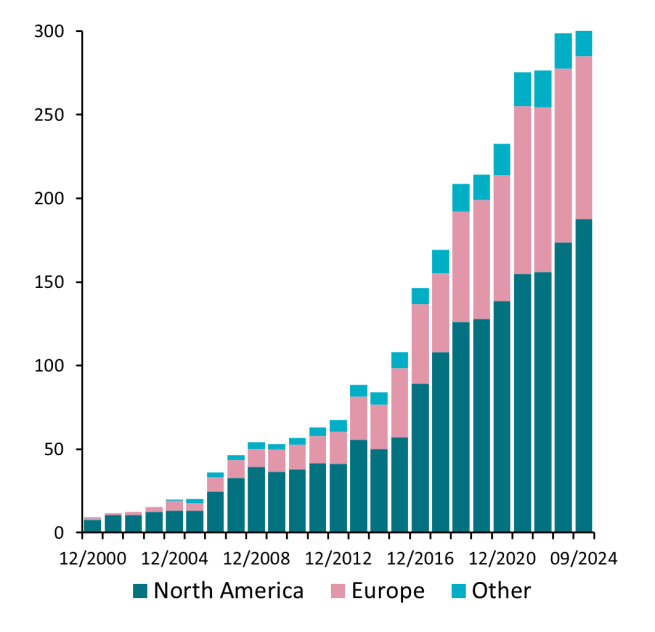

As rates decline, deal flow is expected to pick up, driven by the need to return capital to investors and deploy dry powder. This should support corporate direct lending, which currently holds around $250 billion ready to finance new transactions.

Consumer assets

Consumers are not overleveraged

Contrary to previous periods with elevated market volatility, consumers are entering this period with relatively low leverage, creating a positive backdrop for consumer-related credit assets.

Household balance sheets - particularly in developed markets - remain relatively healthy, supported by years of deleveraging, resilient labour markets, and accumulated savings. While inflation has strained disposable incomes, relatively low consumer debt reduces default risk and helps sustain consumption, though at a slower pace.

Economic uncertainty might weigh on future consumer spending

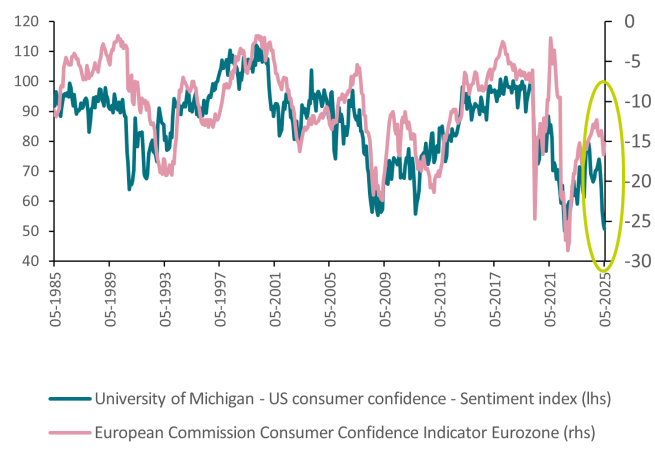

Global consumer confidence has declined since the introduction of tariffs, with US consumers hit hardest. University of Michigan’s survey shows US confidence at its lowest since 2022, even below 2008 crisis levels, potentially dampening spending.

However, strong labour markets and low unemployment across many countries support consumer credit fundamentals, as employment stability helps maintain borrowers' ability to repay loans.

Weaker segments in the US are suffering from elevated rates

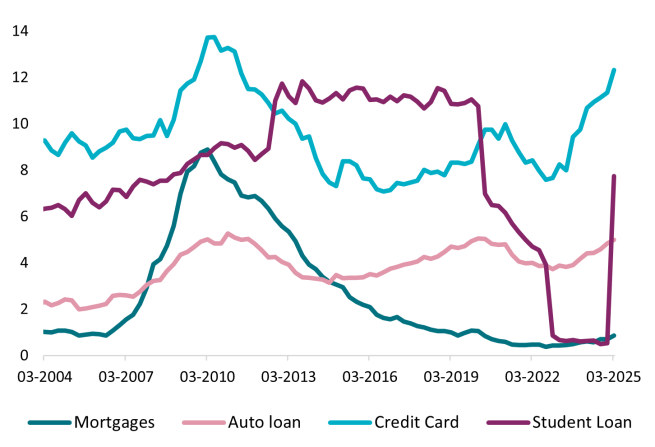

Consumer credit in the US and Europe remains broadly stable despite inflation, trade tensions, and higher financing costs. While delinquencies are rising, they remain below Global Financial Crisis levels. Prime consumer assets continue to perform well, with low and stable delinquency rates.

However, non-prime and non-conforming loans are showing signs of strain, especially among borrowers with weaker credit profiles and less stable income. In the US, credit cards, auto loans, and younger borrowers are particularly affected. The end of the COVID-era pause on student loan delinquencies has further pressured consumer credit.

Tariffs and economic uncertainty are also dampening consumer confidence and spending. As a result, there is growing performance dispersion in consumer credit, prompting a focus on prime exposures and caution toward more vulnerable segments.

Our convictions

- Positive outlook on Credit assets: Central banks - especially in Europe - are easing policies which is supporting economies, and recession risks appear to have subsided. Compared to the US, we are more optimistic on Europe’s outlook which is benefitting from improved economic indicators, lower energy costs, less impact from negative trade policies and supportive fiscal measures.

- Diversification to navigate uncertainty: Growth divergence across regions and increasing performance dispersion between sectors underscores the importance of selective asset allocation. In this environment, careful portfolio construction and robust diversification are essential to manage risk.

- Income will be key: Market volatility remains a key concern. In this context, income generation and income stability should be top considerations as investors review their overall allocations. Liquid alternative credit strategies offer flexibility and responsiveness in turbulent markets while private debt continues to provide attractive yields and downside protection through bespoke structuring and covenant-heavy lending.

Source 1: Bloomberg, AXA IM Alts. June 2025.

Source 2: AXA IM, New York Fed Consumer Panel/Equifax. May 2025. Balance-weighted transition to credit card delinquency among borrowers who were current on all credit card accounts in the previous quarter. A borrower’s utilisation group is determined by their utilisation in the previous quarter.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.