CLO equity - Riding the wave of volatility

As investors navigate a landscape defined by rate uncertainty — one asset class has proven it deserves a larger allocation in investors’ portfolios — CLO (Collateralised Loan Obligation) equity. Once considered too complex or risky for mainstream portfolios, CLO equity is now gaining recognition for its compelling risk-reward profile in today’s ever-changing environment. In 2024, CLO equity was one of the top-performing asset classes and we think there are factors that should continue to drive this performance.

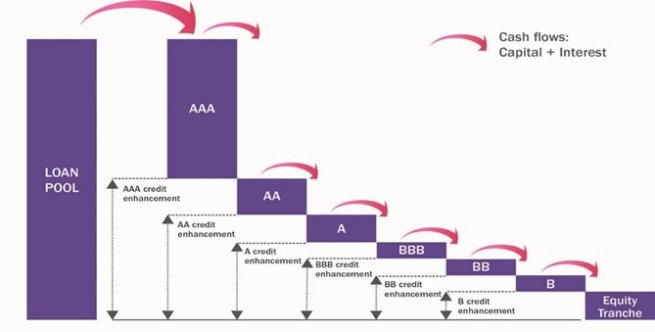

What Is CLO equity?

A CLO is a securitised vehicle that pools together hundreds of senior secured loans, usually made to below-investment-grade (IG) corporate borrowers. These loans are actively managed by CLO managers, and the structure issues different tranches of debt and equity to investors.

At the bottom of the stack is the equity tranche, which has the highest risk-reward characteristics. It receives the residual cash flow after debt tranches are paid and therefore bears the first losses if defaults occur. In exchange, it offers the potential for high internal rates of return (IRRs) depending on the collateralised portfolio of Loans’ performance.

Why has CLO equity performed so well

CLO equity returns are driven by excess spread — the difference between the income generated by the underlying loan portfolio and the total amount paid out to cover the CLO's liabilities, such as interest on debt tranches. This gives them a distinct risk profile compared to debt tranches, which earn fixed margins over reference rates like SOFR or Euribor. Despite credit cycles and macroeconomic uncertainty, CLO equity tranches have historically delivered strong cash flows, with annual returns typically between 13–18%[1]. This resilience stems from the CLO's design: a diversified pool of leveraged loans supported by structural features that protect long-term value.

Over the past years, returns have been at the high end of the historical average, driven by a number of factors:

Attractive entry valuations: CLO equity tranches were trading at steep discounts in late 2022 and early 2023 due to fears of a credit downturn and liquidity pressure. Investors who entered at those depressed levels have since benefited from higher-than-expected cash flows and lower realised default impact than projected.

Increased demand: Institutional investors have increased allocations to CLO equity. With limited new issuance, this has supported secondary market pricing.

Why CLO equity continues to be attractive:

High potential returns with active credit management

CLO equity offers some of the most attractive yields in structured credit, especially compared to similarly rated high-yield bonds or leveraged loan funds. CLO managers actively trade and manage the loan portfolio to improve credit quality, extend the reinvestment period and optimise cash flows. This active management adds an important layer of risk mitigation.

Floating-rate exposure in a volatile rate environment

With uncertainty around future monetary policy both in Europe and the US, investors are increasingly looking for floating-rate instruments to protect against duration risk. CLOs – which are floating-rate – see their income follow the patterns from the rates market.

A better outlook for Europe

There has been a notable divergence between European and US CLO equity distributions, with median European payouts exceeding those in the US over the last quarters. This is partly due to loan repricing from 2024 to April 2025 being more pronounced in the US.

However, there are also more structural drivers. European CLOs can allocate more to fixed-rate assets – typically over 10%, compared to low single digits in the US – allowing managers to benefit from falling rates. Additionally, regional variations in loan default and recovery patterns have influenced return disparities. US default rates should remain higher for as long as the significant difference in interest rates remains.

CLO equity tends to outperform when market risk increases

Some of the best-performing CLO equity vintages are those which were launched shortly before periods of increased risk. Vintages launched before the 2008 financial crisis – or the pandemic shock in early 2020 – have often outperformed CLO debt, primarily due to their greater upside potential during periods of market recovery.

While CLO debt offers more stable, predictable cash flows and downside protection, CLO equity benefits from reinvestment flexibility and the ability to capitalise on market dislocations. During volatile periods, managers can reinvest into discounted, higher-spread loans, significantly boosting the long-term returns of the equity tranche.

As markets stabilise and loan prices recover, CLO equity captures a disproportionate share of the upside through enhanced excess spread and NAV (Net Asset Value) appreciation – returns that are capped for CLO debt investors. This dynamic has led to exceptionally strong performance for pre-crisis CLO equity vintages.

We wrote in our mid-year Alternative credit outlook about how the market volatility that has been brought about by geopolitical tensions and trade wars is not transitory, and that we are likely to see heighted market volatility for some time. In this type of environment, active CLO equity managers are better able to exploit short-term opportunities.

What are the risks?

As the first-loss position, CLO equity tranches are sensitive to defaults and credit deterioration in the underlying loan portfolio. A recession or spike in corporate bankruptcies could reduce or even eliminate equity cash flows in some cases.

Additionally, CLO equity returns can be uneven, depending on reinvestment activity, manager behavior, and prepayment rates.

To mitigate these risks, it’s critical to:

- Invest with experienced and transparent CLO managers.

- Diversify across issuers, geographies, sectors etc.

Outlook and positioning

The current environment presents a strong opportunity for CLO equity investing. From a rates perspective, lower rates in Europe and the US are supportive for corporates as they may translate into a more manageable default environment which is favourable for cashflow performance.

In this environment, we tend to favour long-dated CLO equity tranches with low NAV because a) long-dated tranches are those with several years remaining in their reinvestment period and b) equity tranches with low NAVs trade cheaply because their value already reflects weaker assets and high expected yields, making their prices less sensitive to further market swings.

Additionally, investing early in CLO transactions can offer substantial upside, particularly when combined with participation in the CLO warehouse phase. This phase is where CLO managers purchase loans during the ramp-up period. As they accumulate assets, they also generate carry, which is paid to warehouse investors.

Participating in the warehouse phase enables investors to influence the timing of transactions, facilitating the identification of attractive loans at optimal prices and enhancing value through active trading. This strategic approach can result in increased returns in a fluctuating market environment.

[1] AXA IM Alts. July 2025. For illustrative purposes only. Past performance is not a guide to future performance.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.