The evolution of Multi-Private Credit strategies in alternative markets

A $40trillion market opportunity

Since the Global Financial Crisis, banking regulation has reshaped the credit landscape. Capital adequacy rules, liquidity coverage ratios and stress testing frameworks have pushed banks to reduce their balance sheet exposure to corporate and real estate lending – even when those loans are high-quality. This structural retreat has created a financing gap, particularly in segments that require long-term, flexible capital.

Enter Private Credit. Unburdened by the same regulatory constraints, alternative lenders have stepped in to fill the void. What began as a niche strategy has evolved into a $40 trillion1 global market, spanning direct lending, Asset-Backed Finance and structured credit.

Yet as the market matures, so do investor expectations. The next frontier is not just access to Private Credit but access that is scalable, diversified, and aligned with the liquidity needs of different investor types.

The rise of Multi-Private Credit

Multi-Private Credit strategies in the private asset space are actively managed portfolios that combine multiple Private Credit segments within a single investment vehicle. Rather than focusing on a specific credit type, they allocate across a broad spectrum of credit risk and liquidity profiles. By allocating across direct lending, Asset-Backed Finance and selected public credit exposures, Multi-Private Credit strategies aim to capture relative value across the cycle while mitigating concentration risk.

In general, Private Credit offers investors structural protection through covenants, collateral and subordination, and enhance downside mitigation compared to public high-yield debt. But more importantly, the breadth of the Private Credit landscape allows for a high degree of diversification, both in terms of exposure and income sources.

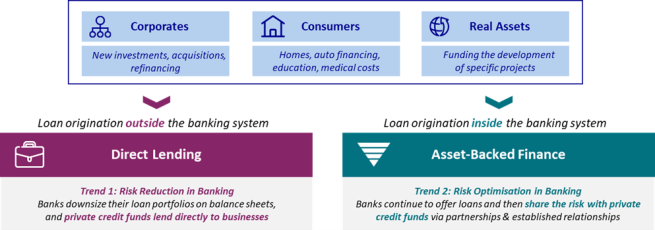

Just to give a few examples, direct corporate lending provides exposure to mid-market companies through senior or unitranche loans, typically with floating rates and conservative leverage. Asset-Backed Finance, ranging from ABS and CLOs to Significant Risk Transfer (SRT) structures, offers access to granular pools of consumer and corporate loans.

The importance of established partnerships with banks

Despite the trend of bank disintermediation in the corporate lending market, banks and Private Credit lenders still collaborate to address funding gaps in the market. Banks typically handle origination, leveraging their extensive client relationships and industry expertise to identify and structure deals. Private Credit investors then provide the credit risk capital, often sharing or taking on the debt alongside the bank’s involvement.

A crucial differentiation in the Private Credit market is a long track record. Long-standing, experienced Private Credit investors tend to have more established partnerships, built on proven collaboration. These long-term partnerships allow for a continuous flow of high-quality deal opportunities, with banks benefiting from risk sharing and private lenders gaining access to trusted origination channels.

Evergreen structures: liquidity meets discipline

Historically, Private Credit has been accessed through closed-end funds - vehicles that raise capital through a one-time offering with a fixed number of shares, meaning flexibility for the investor is limited. These opportunities were largely reserved for large institutions due to high ticket size thresholds, illiquidity with multi-year lock-ups and operational hurdles such as having to meet capital calls.

Evergreen vehicles - which allow for continuous capital inflows and outflows – offer an alternative with frequent liquidity while maintaining exposure to the same underlying assets. The structure is particularly well suited to Multi-Private Credit strategies. The diversity of instruments – some with shorter durations, others with predictable cash flows –generates regular liquidity. As opposed to closed-end funds, investors benefit from immediate deployment into existing portfolios, regular income distributions and the ability to scale exposure over time.

A new chapter for Private Credit allocation

In today’s volatile public markets, Private Credit can provide investors with stable income, low correlation to public markets and a buffer against inflation as a large share of the market is made up of floating-rate instruments.

But the real innovation lies in the convergence of structure and strategy. By combining the breadth of Multi-Private Credit with the accessibility of evergreen structures, investors gain access to an investment vehicle where capital can be scaled more easily.

As banking disintermediation continues and credit markets evolve, the question is no longer whether Private Credit belongs in a portfolio. The question is how best to access it. In that context, Multi-Private Credit evergreen vehicles may well represent the next generation of Private Credit investing: flexible, institutional in quality and built for the long term.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.