Flex Equity : The case for Europe’s mid-market

- Europe’s mid-market companies offer attractive investment opportunities due to their solid cash flows, potential for innovation, lower entry multiples and multiple exit possibilities.

- Flex Equity solutions provide flexible, hybrid financing options tailored to the specific needs of these companies, balancing debt and equity features to address challenges like cash flow management and alignment of interests.

- The mid-market segment benefits from strategic investor influence and diverse exit pathways, making it a compelling environment for flexible capital strategies like Flex Equity to unlock value and support business growth.

Europe’s mid-market – comprising businesses typically valued between €50 million and €500 million – has become increasingly attractive to investors, nearly doubling in size over the past decade[1]. These companies often fall below the radar of large Private Equity (PE) and credit funds but offer highly attractive fundamentals: strong cash flow through longstanding, established businesses (many of which also operate in defensive sectors), great opportunities for product innovation and potential to scale up from current markets.

Coupled with valuation dynamics – European mid-cap businesses tend to trade at lower multiples than both their US counterparts and large-cap European firms – this segment has caught the attention of investors over the last few years. One way in which to access these opportunities are through Flex Equity solutions.

What is Flex Equity

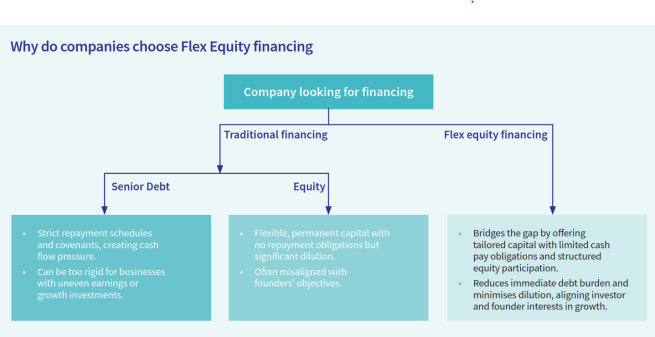

Flexible Equity – commonly referred to as Flex Equity – sits at the intersection of traditional equity and bond financing. It provides financing solutions with hybrid characteristics – often structured as preferred equity, convertible debt or structured equity – and adapted to the needs of the company.

For example, an established industrial company with steady cash flows and a management that is unwilling to give up any control of their company will likely prefer more debt financing.

As the illustration below demonstrates, Flex Equity provides innovative solutions to some of the traditional financial challenges faced by companies. One of the primary issues with traditional debt is the burden of cash flow and debt servicing, especially during periods of growth or uncertainty. Additionally, conventional equity structures can sometimes lead to misalignment between founders and investors, as their interests and expectations may differ: founders often aim for long-term growth, while investors may focus on short-term returns. Flex Equity addresses this potential misalignment by offering a more flexible financing approach that aligns incentives through mechanisms such as performance-based rewards or tailored conversion terms. Additionally, founders and managers – especially in the case of primary deals – will naturally favour non-dilutive instruments to maximise their share of the value creation.

For companies, Flex Equity offers bespoke capital solutions adapted to their specific needs. For investors, Flex Equity is designed to offer a return profile blending equity-like upside and debt-like downside protection.

This financing solution has gained prominence in the past decade, particularly among PE sponsors (PE Fund managers) and growth-oriented businesses seeking non-dilutive or minimally dilutive capital. It’s especially relevant in situations where a) traditional lending is constrained, as bank lenders have faced stricter capital requirements and lower risk boundaries, and b) full equity issuance is undesirable.

The European mid-market landscape

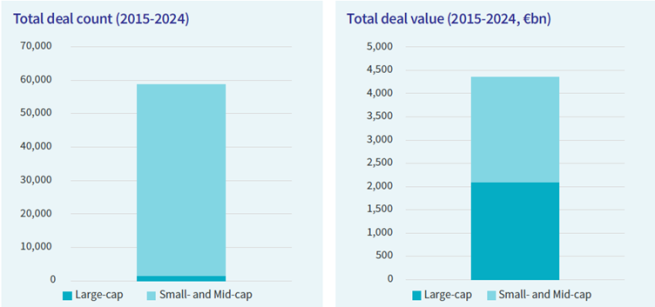

Mid-market deals make up a large majority of all European PE deals. While large-cap deals continue to dominate headlines, it’s the mid-market where transaction volumes are more abundant, valuations more attractive, and competition for deals less intense. While it’s a market with a great depth of opportunities across sectors, it’s also more specialised than the large cap market. As result, investors need deep market knowledge, a wide network and extensive experience to source the most attractive deals.

Valuations and entry multiples

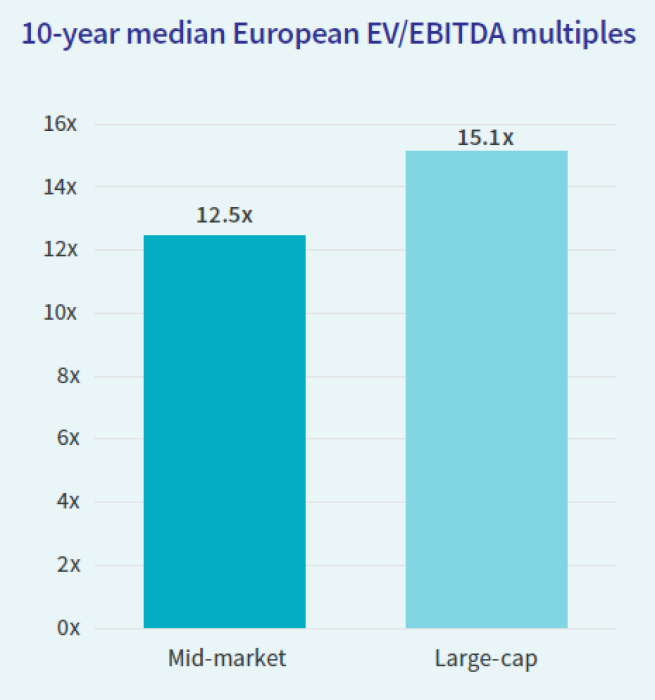

European mid-market companies have historically traded at lower EBITDA multiples than their large-cap peers. This valuation gap presents attractive entry points for investors seeking value-driven strategies, and we see no indicators of this changing anytime soon.

Less competitive market dynamics

Unlike the highly competitive US market, where sponsor-driven deal flow is saturated and multiples are elevated, Europe’s mid-market remains relatively fragmented. There are also fewer Flex Equity providers, and many deals are bilateral or sourced through local relationships. This means that buyers in this space are more specialised and terms for investors can be more favourable.

Leverage and capital efficiency

Another de-risking factor is that mid-market businesses are generally more conservatively levered than their large-cap counterparts. This provides a safer capital structure for Flex Equity investments and room to layer in moderate debt if needed. It also creates space for creative structuring, such as dividend recapitalisations, which can further enhance returns.

Influence and control advantages

Investors are increasingly recognising the strategic advantage of having a meaningful voice in company direction. Unlike in large-caps, where companies often set the agenda, investors in mid-market companies are positioning themselves to influence key decisions – whether through board representation, veto rights, or reporting covenants – even without holding a controlling stake.

This level of engagement fosters stronger alignment with management, facilitates more informed decision-making, and ultimately enhances the capacity to de-risk investments over the long term. Such strategic influence not only adds value but also underscores the evolving role of Flex Equity in shaping resilient and well-governed mid-market enterprises.

Exit and distribution potential

Lastly, a key advantage of mid-market vs large-cap investing is the variety of exit options. Companies may grow into private equity targets, pursue IPOs or attract strategic buyers. Flex Equity instruments can be structured with call features, redemption options, or put rights to ensure timed liquidity.

Additionally, because of the hybrid nature of the instrument – combining features of both equity and debt – investors often receive regular income through dividends or interest payments. This improves cash flow and helps reduce the J-curve effect of negative returns common in PE investments before profits materialise. This makes the investment more attractive for yield-focused portfolios seeking steady income and quicker positive returns.

Short- and long-term drivers

In addition to the factors already listed, in the shorter term European mid-market firms also benefit from renewed interest from investors looking for opportunities that are more insulated from trade wars as well as benefiting from increased European domestic defence and energy spending.

The European opportunity

Flex Equity is particularly well-suited to Europe’s mid-sized companies, many of which face capital needs that fall between traditional debt and full-blown Private Equity investment. These businesses often need €10–100 million to support expansion, acquisitions or ownership transitions. For a large buyout fund, which typically raises substantial capital to acquire and take control of large companies, the opportunity might be too small. For traditional lenders the opportunity might be too intricate and bespoke.

An increasing role

The combination of lower competition, favorable valuations, greater influence, and structural downside protection makes this segment uniquely suited to flexible capital strategies. As traditional bank lending remains constrained, companies seek non-dilutive alternatives to fuel growth, and LPs look for increased DPI (Distributions to Paid-In Capital), Flex Equity will play an increasingly important role in unlocking value across Europe’s vibrant mid-market landscape.

[1] Invest Europe. November 2024. Data for 2013 to 2023.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.