Disintermediation and market repricing create opportunities in Alternative Credit

Key takeaways

- Markets are adapting to a new cycle of higher yields, less available liquidity and elevated volatility.

- The trend of bank disintermediation will continue to create opportunities for alternative lenders, especially in CRE debt.

- Repricing in public and private markets has created attractive entry points.

- Credit selection and active risk management will be key amid a higher dispersion of returns in Alternative Credit.

- Enhancing diversification through uncorrelated asset classes within alternative credit markets will be key to weather volatility and interest rate risk.

While 2023 was a challenging year, with markets swinging between fear of recession and expectations of a soft landing, Alternative Credit markets proved their robustness. Many of these challenges will remain in 2024, but we expect structural trends to be supportive of Alternative Credit performance in this higher-for-longer environment.

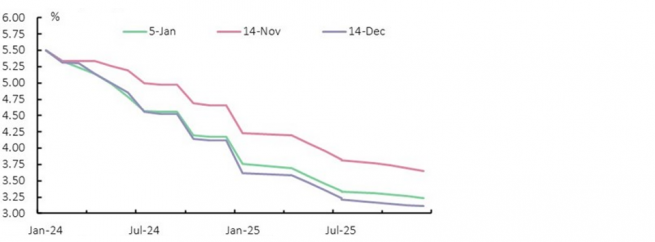

Rate cut expectations are too pronounced

We believe three key themes will dominate Alternative Credit markets as we move into the next phase of the economic cycle, which in the short-term will be dominated by interest rate expectations. While we expect rates have peaked, we believe they will remain higher for a longer period than we thought six months ago – and than the market currently expects. Yes, weakness in Chinese economic growth contributes to global disinflation. But the US labour market is still tight, and the Fed is wary of re-triggering inflation by loosening financial conditions too quickly.

The three key themes which will affect Alternative Credit markets in 2024

1. Adapting to higher yields

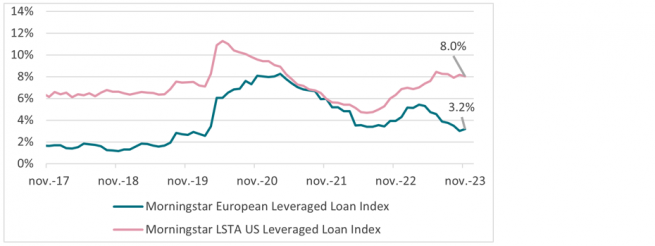

Global markets are still adapting to a new cycle of higher interest rates and central banks will continue to reduce market liquidity well in to 2024. The higher-for-longer yield (rates and spreads) environment should result in performance dispersion across underlying asset classes. Attractive opportunities will arise but selectivity will be key.

2. Disintermediation trend continues amid bank lending retreat

Fed and ECB lending surveys show banks tightening their lending standards, in part driven by higher capital costs. This means banks will lend less to the economy, reinforcing the role of alternative credit as a key source for companies to fill this funding gap. To give some examples, private credit is used for direct lending, CRE debt or Infrastructure debt. With banks retreating from these types of lending, it also means private lenders can offer more attractive returns to their investors, due to the decreasing number of competitors.

3. Market volatility is here to stay

While markets are pricing in a number of rate cuts this year, persistent headwinds remain, such as increasing geopolitical risks, weaker economic growth and a rising default outlook due to higher lending costs. Because of this, market volatility is likely to remain elevated, especially given the uncertain outlook for central banks’ monetary policy. This can create attractive entry points, but diversification will be essential.

Digging deeper into defaults and delinquencies

In our opinion, corporate defaults will remain low (around their historical average). One reason is that they did a good job overall in extending their debt profiles during the low interest rate period. This is true both in the US and Europe, as can be seen in the table below, where a large share of corporates don’t have loans due until 2028.

Despite this, loan downgrades outpaced upgrades during 2023, increasing the proportion of CCC-rated companies, notably in the US. But dispersion between sectors is high and we consequently think that active sector selection will help to minimise downgrade risk.

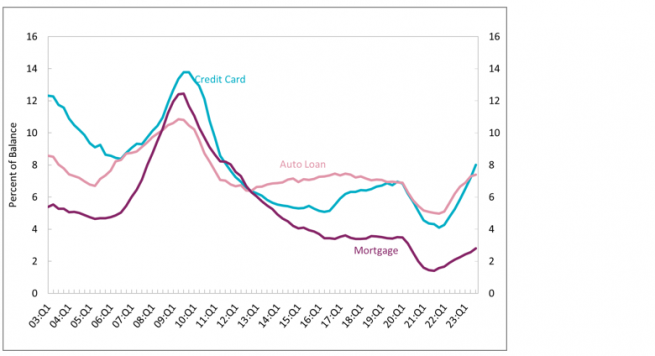

Consumer resilience will be tested

While consumer spending was one of the main factors explaining the resilient global economic growth in 2023, households are now running out of excess savings. We expect consumer assets to be significantly impacted by this. Consumer assets have been supported by relatively low unemployment rates in Europe and the US, but we have started to see a slightly negative trend over the past few months. This, combined with rising rates, has started to have a negative impact on delinquencies – especially in US rate-sensitive sectors such as auto loans and credit cards for which ‘early delinquencies’ (30 days) are increasing. This is a usually a good indicator of a looming economic slowdown.

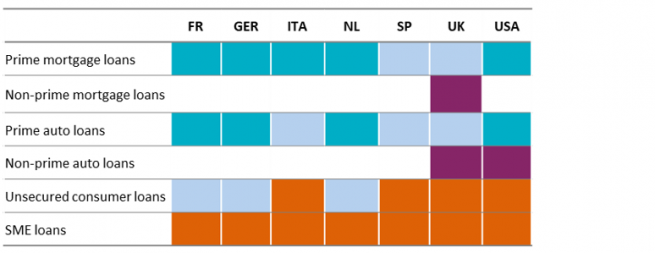

In light of this deteriorating data, we believe unsecured consumer loans and non-prime loans are most at risk. Regionally, we see UK assets as more vulnerable than their eurozone counterparts as consumers have been harder hit by rising energy prices, they face higher interest rates and inflation has fallen much quicker in the Eurozone that in the UK.

Structural changes and highly attractive entry points in the real assets sector

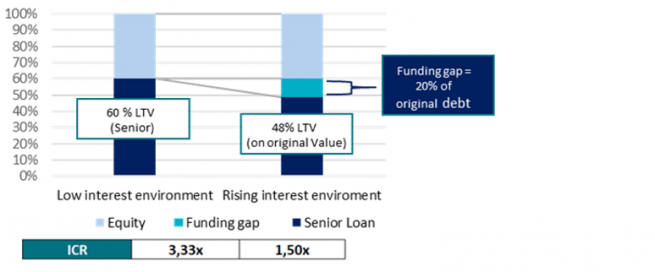

Real Estate lending is one of the areas in which the role of alternative lenders has become very pronounced. The withdrawal from banks has led to a funding gap and the high interest rate environment has reduced the LTV ratio banks are willing to accept. While rates have likely peaked, we expect them to remain elevated for longer and this should continue to create important opportunities particularly in the CRE debt sector, but also in infrastructure which provides an important inflation hedge and low correlation to other asset classes.

A bumpy ride ahead but with plenty of potential rewards

As we move through 2024, we expect the opportunity set for Alternative Credit to be broader as its importance in financing the real economy becomes more pronounced. Many alternative lenders will be supported by the continued disintermediation of banks but diversification and selectivity will be required to navigate an increasing number of defaults, slowing growth and less-available consumer capital. We expect a bumpy ride for markets but believe that this can create attractive opportunities for long-term investors.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.