High volume markets – a different way to deliver impact

- Accessibility – and affordability – of quality healthcare is a global concern, and changing lifestyles are exacerbating these problems.

- Private capital is needed to deal with these challenges, but it has historically largely focused on complex and costly areas of the healthcare sector such as biotech.

- We believe the focus should instead be on effective, easy-to-use and affordable products that are distributed not only in high-income markets, but in global mass-markets with enough scale to deliver tangible impact.

Healthcare challenges abound

Over half the world’s population - about 4.5 billion people – lack access to essential health services. Projections predict a global shortfall of 10 million healthcare workers by 2030, with the largest gap in the poorest countries

With more interconnected countries and a more globalised world, the risk of healthcare systems being burdened by global pandemics is also rising. What role can private capital play in tackling these enormous challenges?

Globalisation is driving the rise in NCDs

Covid demonstrated how quickly an epidemic could turn into a pandemic, but highly transmissible infections are not the only health issues that have spread throughout the world. In modern history there has been a global increase in NCDs including cardiovascular disease, diabetes, cancer and chronic respiratory disease. In many cases, their spread has been linked to globalisation or urbanisation and the lifestyle changes associated with it.

Demographic and lifestyles changes are straining healthcare systems

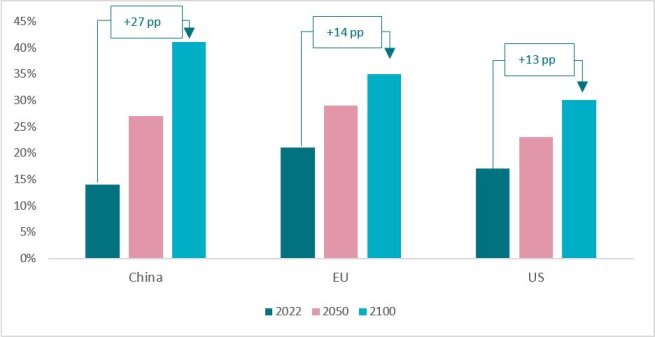

Aging populations have been an issue in high-income countries for several decades, and it is now also becoming a concern in middle- and low-income countries. In 2025, there will be a higher proportion of people aged 65+ in China than in the US. Worse, aging populations are often followed by shrinking populations, meaning fewer people active in the workforce to fund public healthcare.

Aging populations, not only in high-income countries

Healthcare spending is increasing globally – but large disparities remain

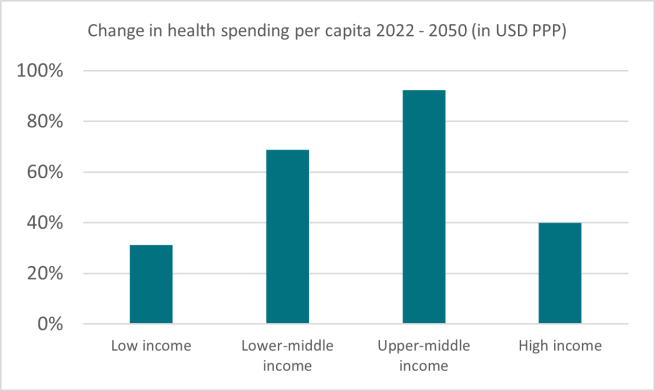

These changes lead to higher healthcare expenditure and needs for investments, especially in affordable healthcare. The largest rise will happen in upper middle-income countries, such as Mexico, Brazil, China and South Africa, where it will almost double by 2050, followed by lower-middle income countries. Middle income countries represent huge markets, accounting for 75% of the total global population

Private capital tends to focus on biotech

So far, private capital has largely focused on specific areas of the healthcare industry such as biotech firms and advanced medical equipment that require specialised medical staff and expensive complementary equipment. These markets are characterised by high research and development costs, with investors hoping to translate these into the very few that succeed and become highly profitable products protected by patents and limited competition.

But what if the aim would instead be to deliver simple yet highly effective, mass-market products aimed at improving and saving lives, while benefiting large groups of underserved communities? To generate significant returns through economies of scale and low-cost production chains, rather than through high-priced products with very high R&D costs and limited social impact.

Impact in countries where growth potential is the greatest

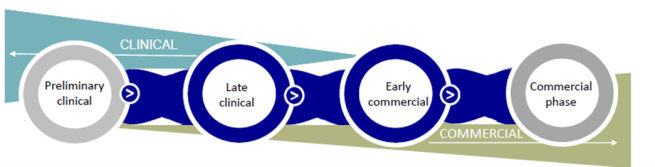

We focus on global markets by investing in companies at the late-clinical or early-commercial stage, that can deliver high volumes of affordable products which do not require highly trained staff or significant complementary equipment. This is in contrast to the preliminary clinical stage, which is often the focus for many Private Equity investors.

High-volume countries tend to have significant growth potential and rising populations. Crucially, many also have sufficient public spending capacity to afford the products and services being developed by the companies we invest in.

Only a small number of funds have a focus on high-volume markets – i.e. large, middle-income markets that allow for significant economies of scale. Those that do are typically local emerging market funds focused on digital innovation rather than products that solve for global health issues. The funds that do invest in high-volume markets generally do not have the capital to invest in companies that have the potential for global reach, instead focusing on stimulating the local economy and communities.

We see targeting global high-volume markets as an important way to deliver impact where it really benefits large populations, and where the scale that can be achieved can deliver accessible prices for the end consumer as well as attractive returns for investors.

How our strategy works in practice - MNHI

Maternal Newborn Health Innovations (MNHI), is a US-based public benefit corporation established to reduce the impact of maternal and newborn mortality worldwide. In 2023, MNHI launched a new medical device designed to reduce maternal and newborn deaths and complications resulting from prolonged or complicated second-stage labour during childbirth.

Approximately 10-15% of childbirths (13-19 million annually) are prolonged and difficult, creating risks to mother and baby. Approximately one million infants die each year from complications related to premature labour, according to the WHO. Many of these deaths and complications could be prevented with better interventions.

Current interventions to facilitate delivery in prolonged/difficult labour are limited to forceps and suction. Both approaches are complex and can lead to bruising, fractures, lacerations and other complications. As a result, they are not widely used.

MNHI has developed a simple, effective device that can facilitate natural delivery of infants without the adverse events seen in existing products. We believe this can lead to utilisation in global markets, reducing infant deaths in low- and middle-income countries where most deaths occur, and decreasing the need for C-sections in high-income countries.

AXA IM provided funding to help MNHI work toward regulatory approval in Europe, which will then lead to introduction of the product in global markets. On April 4th this year, the company received its CE Mark (European approval) and will begin commercial efforts in the second half of this year.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.