2025 Alternative Credit outlook – A tale of two trajectories

Key takeaways

- Economic divergence between Europe and the US will necessitate different monetary policies, impacting growth and default rates, while generating new investment opportunities.

- Growth in private credit is expected to continue, providing investors access to a broader range of assets and diversification.

- High levels of policy uncertainty and geopolitical risks suggest an increased likelihood of elevated volatility and greater variations in returns across asset classes and regions.

Despite ongoing geopolitical tensions, 2024 delivered strong performance across credit asset classes as central banks have managed to reduce inflation without triggering a recession. In 2025, central banks should continue their rate cutting trajectory, albeit at very different speed. In this environment, we identify three key themes that will influence markets over the next year.

- Economic divergence of the US versus the rest of the world

US economic data has outperformed European data. While the US is expected to maintain dynamic growth, there is a risk of persistent high inflation due to President Trump’s proposed tariffs and immigration policies. This may limit the Federal Reserve’s (Fed) ability to further ease their monetary policy, causing US interest rates to remain elevated for a longer period, which could negatively affect businesses and household finances.

In Europe, the overall growth outlook is weaker, but nuances exist within this economic divergence. While the two largest Eurozone economies face political uncertainty, countries like Spain and Portugal have experienced dynamic economic activity over the last two years. In this context, the European Central Bank (ECB) might need to accelerate its easing cycle to support the economy.

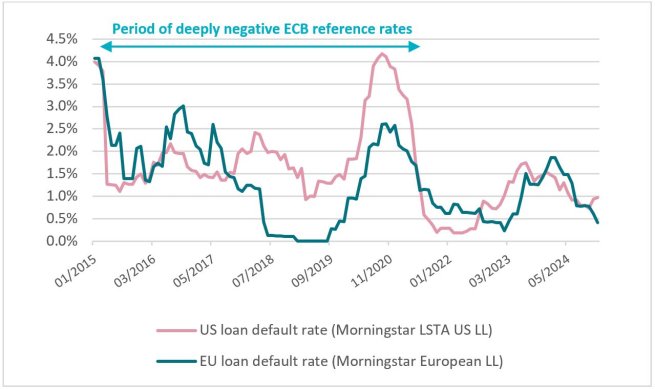

As a result of the difference in interest rate policies, we are already seeing higher corporate default levels in the US than in Europe, and this difference is likely to remain for as long as the interest rate trajectories diverge. Historically this was the case during the long period of deeply negative ECB rates during the last decade where US loan default rates were higher, as illustrated in the chart below.

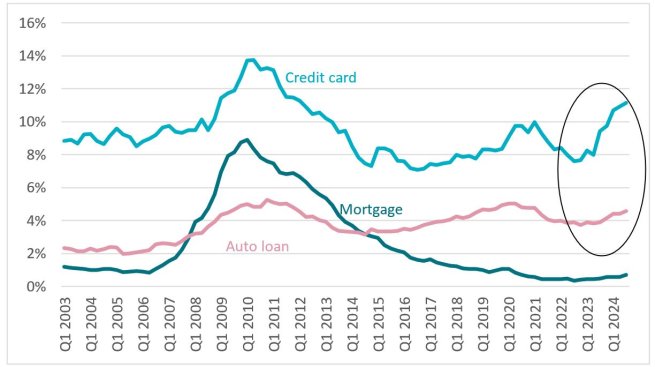

In the US, elevated rates are already impacting consumer assets negatively, with deteriorating indicators such as credit card and auto loan defaults, as illustrated in the chart below.

However, globally, our outlook on consumer assets remains positive as household finances are generally strong in both the US and Europe. But investors should expect more varied performance and avoid weaker sectors of the economy, which will continue to be adversely affected by high rates. Diversification will remain a key factor in portfolio construction.

2) Ongoing bank disintermediation

Private credit has experienced significant growth over the past decade due to banks‘ retreat from lending. Despite potential deregulation from the US administration, we expect this trend to continue as banks seek to optimise their balance sheets and safeguard their long-term profitability. Previously, most of the growth in the private debt market was related to corporate direct lending. The new form of bank disintermediation provides investors access to a broader and more diversified investment universe, including Asset-based finance, consumer and real assets as well as specialty finance - such as Capital Call facilities and Significant Risk Transfer (SRT).

The Corporate direct lending market is estimated to be worth less than $2 trillion, while the Asset-based lending market is estimated at around $40 trillion[1]. Private credit continues to grow by filling this funding gap, and we expect this trend – which is only at an early stage - to accelerate in 2025. This growth will create even more opportunities for investors to diversify, while benefitting from ongoing structural trends.

3) Resilient fundamentals but outlook more uncertain

After a strong market rally over the last two years, spreads on credit markets have narrowed. However, policy uncertainty, fiscal deficits, and ongoing geopolitical risks are making the market outlook increasingly uncertain.

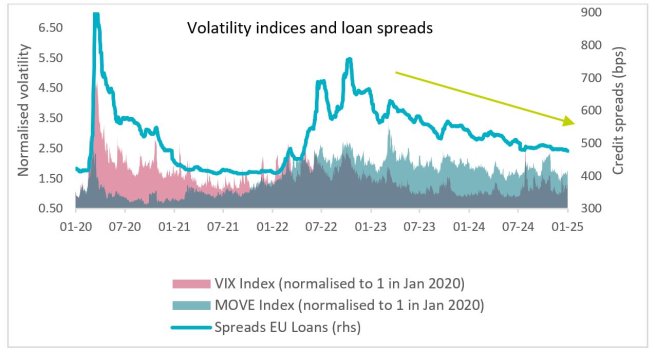

This uncertainty is best illustrated by the divergence of volatility regimes. While the global market rally has led to very low implied equity volatility, as shown by the VIX index, the MOVE index, which measures implied volatility of US treasuries, has increased significantly over the last two years.

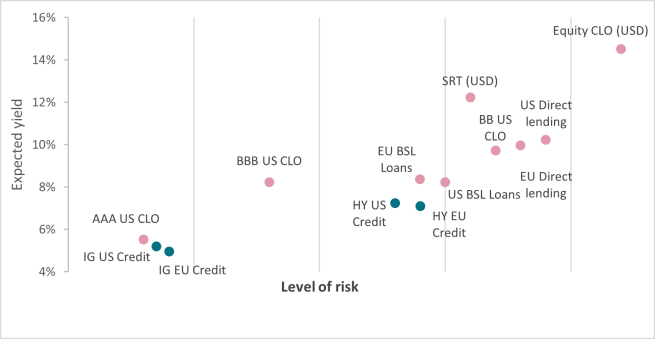

So where should investors look for superior returns without taking on excessive risk? In this environment – characterised by greater dispersion of returns between countries, regions, asset classes and prime and non-prime assets - investors might want to diversify their portfolios and allocate to areas that can deliver better yields than traditional credit without compromising the portfolio quality. As shown in the example below, many liquid alternative credit asset classes can offer better relative value for equivalent credit quality.

Past performance is not an indicator of future performance.

Summary

Resilient growth implies a pro-risk perspective. We maintain a positive outlook for credit assets, supported by robust fundamentals, accommodative monetary policies from central banks, and a growth-oriented environment. However, after a strong performance in 2023 and 2024, public credit markets have become tight.

With the ECB and the Fed following different paths, this divergence may increase the risk of defaults in weaker market segments. Persistent geopolitical risk, inflationary pressure, policy uncertainty and rising fiscal deficits may further contribute to increased volatility in long-term rates.

We anticipate growing idiosyncratic risk and performance dispersion across asset classes. The differentiation between countries and regions presents both opportunities for portfolio diversification and construction, as well as the potential for investors to seek diversification beyond traditional credit markets. This development underscores the importance of credit selection and local market expertise.

In summary, we believe that liquid Alternative credit and Private debt offer better value for income generation and diversification purposes in 2025. Given the current environment, carry, rather than capital appreciation, is expected to drive returns.

[1] AXA IM Alts, Feb 2025.

[2] CLO in USD, JP Morgan CLO indices, US credit IG and HY: ICE Bofa Corporate Credit indices, Broadly Syndicated Loans (BSL) US and EU: JP morgan Loan indices, Equity CLO: AXA IM estimates, US and EU Direct Lending: AXA IM estimates.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.