Alternative credit outlook: navigating an evolving landscape

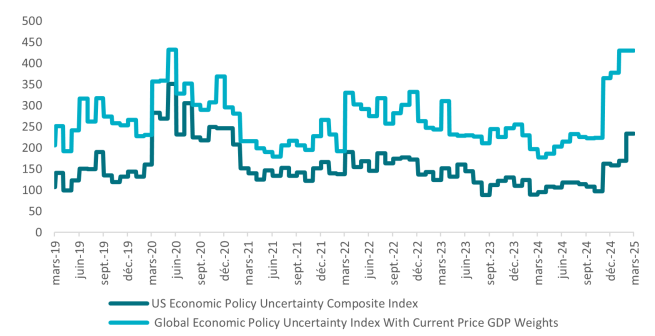

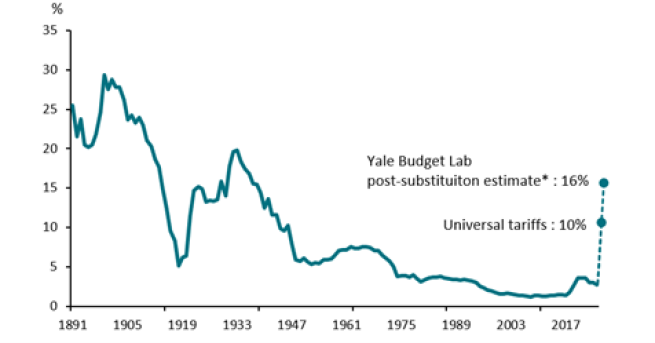

Shifting macroeconomic conditions, policy uncertainty and sectoral divergences have disrupted the outlook for 2025. If the US persists with tariffs, these are likely to fuel inflation and significantly impact growth rates.

In the US, the Fed is trying to adjust to inflation and recession fears, and investors must navigate a much more uncertain landscape. Meanwhile, Europe’s relatively stable political environment compared to last year provides a degree of policy reassurance.

Risk management: quality and diversification

Significant macroeconomic and geopolitical uncertainty persists, warranting a diversified investment approach and careful portfolio construction. While corporate and consumer credit fundamentals remain generally resilient, market sentiment has shifted rapidly because of tariffs and policy risk.

Performance dispersion across sectors will consequently be greater. Investors should favour high-quality assets, maintain sectoral diversification and adapt to evolving macroeconomic conditions as volatility will be a key theme throughout 2025.

Corporate assets: a sectoral and geographic divergence

Defaults: A gradual return to historical norms

Default rates in corporate credit markets are set to rise towards historical averages after a prolonged period of below-average defaults. However, the trajectory is not uniform across sectors, with varying levels of stress depending on industry-specific factors.

The US is already experiencing higher default rates compared to the Eurozone, a reflection of the divergent monetary policies. The Federal Reserve’s (Fed’s) higher-for-longer interest rate stance is likely to persist as they seem unwilling to budge to recession fears, especially given the inflationary uncertainty caused by potential tariffs.

These elevated rates have and will continue to exert greater pressure on US corporates relative to their European counterparts. However, despite the rise in defaults the amount of debt recovered from these defaults has rebounded towards historical averages, having declined in 2023.

Quality will matter: the impact of policy and interest rates

The quality of corporate credit is under pressure, with downgrades continuing to outpace upgrades both in the US and in Europe. High interest rates have weighed on corporate balance sheets, especially in rate-sensitive industries. However, while credit spreads have widened due to increasing tariff and policy uncertainties, the magnitude remains moderate. This reflects investor confidence in credit fundamentals, albeit with an increasing preference for defensive sectors.

M&A and LBOs: Europe healthier than the US

While expectations of increased activity have grown more negative, mergers and acquisitions (M&A) and leveraged buyout (LBOs) activity in Europe is expected to be more dynamic in 2025, particularly in the Mid-cap market. This will be driven by anticipated interest rate cuts by the European Central Bank (ECB), which should facilitate deal-making and refinancing activity. The volume of dry powder peaked in 2023 and remains elevated, which bodes well for mid-cap private equity-backed credit transactions and opportunistic credit investments.

Volatility and repricing – more defensive positioning justified

Market volatility has led to a repricing of liquid alternative credit assets including leveraged loans, collateralized loan obligations (CLOs) and asset-backed securities (ABS). This has created opportunities for investors to acquire high-quality assets at attractive valuations. However, private credit markets have yet to undergo a similar repricing. If market weakness persists, the private credit sector may face increased valuation pressure, necessitating a more careful portfolio positioning, with a focus on more defensive sectors.

Consumer assets: resilience amid growing challenges

Household finances and debt trends

Globally, household finances remain in good shape, yet early signs of weakening are emerging. While household debt continues to trend lower, certain consumer segments are facing increased financial stress. The divergence between prime and subprime borrowers is becoming more pronounced, with prime credit performance remaining robust while delinquencies rise among US subprime borrowers.

Notably, US consumer rate-sensitive asset classes such as credit cards are experiencing a rise in delinquencies, reflecting the impact of prolonged high interest rates on discretionary spending. This trend underscores the importance of focusing on high-quality consumer credit assets while exercising caution in riskier segments.

Our convictions

Credit outlook: constructive but selective

Despite near-term uncertainties the outlook for credit assets remains positive, supported by central bank easing in Europe and a resilient macroeconomic backdrop. However, the divergence between prime and non-prime credit performance is expected to persist, reinforcing the need for a quality-focused approach.

Sectoral differentiation and geographic preferences

Performance dispersion across sectors is likely to remain a defining theme. Defensive, non-cyclical sectors such as pharmaceuticals, medical devices, and utilities offer greater stability in a volatile market. Conversely, sectors vulnerable to tariffs and weaker consumption—such as energy—are less attractive. The US administration’s focus on maintaining lower oil prices to curb inflation further weighs on energy sector prospects.

Regionally, Europe is expected to outperform the US in credit markets due to lower political uncertainty and stronger fiscal support for defence spending. However, much of the economic boost from investment in defence will materialise gradually, requiring a long-term investment perspective.

Sector-specific insights

- Overweight telecom and media: reforms in US broadcast license ownership restrictions will benefit these industries.

- Underweight energy: weaker consumption, tariff-related risks, and policy interventions to maintain lower oil prices weigh on the sector’s outlook.

- US construction, hospitality, and agriculture face labour challenges: immigration reforms are likely to constrain labor supply in these industries, posing operational challenges and wage cost pressures.

- Positive view on European mid-cap direct lending: given its largely domestic or European exposure, this segment is more insulated from global trade tensions and tariffs.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.