The great reset

The great reset

- CLO resets have grown rapidly over the last year due to a favorable macro backdrop and tighter credit markets.

- Resets benefit CLO equity holders by increasing the lifespan of the CLO vehicle and lowering the financing costs of the CLO portfolio, resulting in higher cash flows for the CLO equity tranche.

- Resets provide CLO Managers with more tools to actively manage their risk positioning, benefitting all CLO investors.

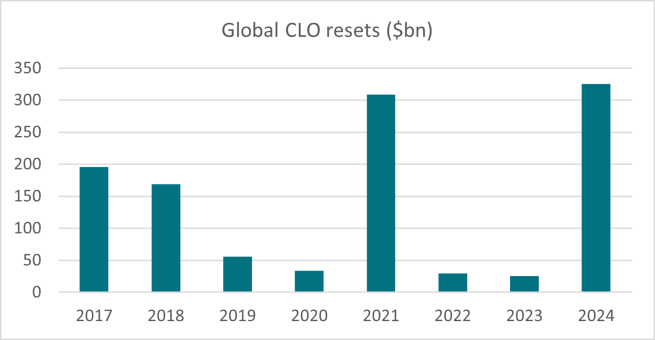

Global CLO (Collateralized Loan Obligations) resets grew by over 1000% year-on-year in 2024[1], spurred by better financing conditions both in the U.S. and Europe. As resets are expected to continue at a high pace in 2025, CLO equity tranche holders should have plenty of opportunities to benefit from this momentum.

What are CLOs?

A CLO is a type of securitisation, in which leveraged loans are bundled and converted into marketable, liquid assets with different risk and interest levels. Investors in the debt tranches receive a coupon composed of a fixed component (the spread) and a floating component (usually 3-month SOFR in the U.S. and 3-month Euribor in Europe), while the equity investors – the tranche with the highest risk – receive the residual cashflows. CLOs support activities such as M&A, dividend recapitalisations and firm expansions – and they own more than half of the global loan market.

What is a CLO Reset?

A CLO reset is a restructuring of an existing CLO. CLOs typically have a finite lifespan, usually between seven to 12 years, with an investment / reinvestment period during which the portfolio manager can actively buy and sell loans to optimise the CLOs performance. A reset allows the CLO to extend the reinvestment period, typically by several years, and adjust other structural features such as fee structures or the underlying loan pool.

In essence, resetting a CLO is like giving it a second life by modifying its original terms to adapt to current market conditions and extend its ability to provide high double-digit distributions while allowing better risk management. There are no theoretical limits as to how many times a CLO structure can be reset, apart from its ability to raise new debt in the market.

How resets benefit CLO equity holders

- Reduced costs: Resets often occur in a low-interest-rate environment, allowing the CLO to refinance its liabilities at cheaper rates. This reduces the financing cost for the structure and enhances the residual cash flows for equity holders.

- Extended cash flow periods: By resetting a CLO and extending its reinvestment period, equity holders can continue to receive cash flows from the portfolio for longer. This prolongs the potential for returns on their investment and even often increases it.

- Optimising loan portfolios: During the reset, managers can restructure the loan portfolio to take advantage of prevailing market conditions, such as tightening credit spreads or reduced default risks, which can further improve returns for equity holders.

Why resets are rising

Resets are at record highs, with over $325bn worth of resets in 2024, after nearly coming to a halt in 2022 and 2023 due to rising rates and wider credit spreads.

The rapid growth is largely driven by improving market conditions, but there are more factors at play, such as:

- High loan supply: The availability of leveraged loans has remained robust, creating opportunities to reset and redeploy capital into high-yielding assets.

- Aging CLOs: Many CLOs issued in the mid-2010s reached - or are nearing - the end of their reinvestment periods, making resets a logical choice to extend their utility.

No indications of a slowdown

While rate expectations – especially in the U.S. - have changed from a rapid decrease to higher-for-longer, rates are substantially lower than their local peak in 2023/2024 on both sides of the Atlantic. As markets are pricing in further cuts in both Europe and the U.S. this year, resets should continue to increase.

We see the higher-for-longer factor as a potential headwind for CLO holders, since corporates may still face elevated financing costs and get limited relief from falling rates. CLO equity holders are directly impacted by any deterioration in credit quality - as it impacts the cashflow generation of the pool of loans managed within the CLOs.

However, corporate default rates remain in line with historical averages as consumer data has remained strong throughout the period of elevated rates. Heightened market volatility brought about by an evolving geopolitical landscape could also pose challenges to corporations seeking to restructure their loans during resets.

The wider case for CLOs

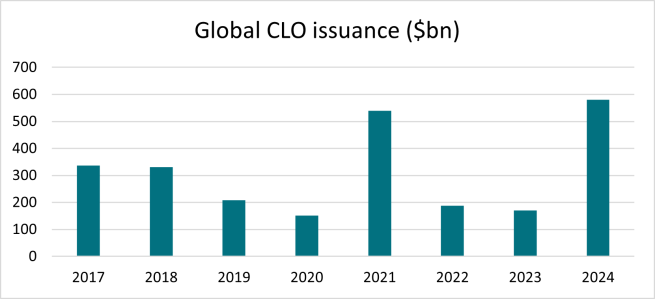

The CLO market has shown a very strong momentum over the last few years, notably due to increased optimism regarding credit conditions, but it also benefited from a favourable relative value compared to traditional Credit markets. As a result, investor appetite kept up with the increasing issuance volume. In 2024, new CLO issuance reached $255bn globally, growing by 75% from the year before[2], with demand driven by a need for higher-yielding investments amid high inflation.

As issuance continues to rise and outstanding amounts grow, CLOs improve their liquidity and marketability and thereby attract more investments. This could prove supportive to CLO credit spreads as well as loan spreads, the necessary raw material for CLO vehicles. For existing CLO investors - and specifically CLO equity holders - this may boost the market value of underlying loans in their portfolios, as well as their tranche valuations.

Summary

CLO resets are a critical mechanism in the CLO lifecycle, allowing existing vehicles to extend their utility and adapt to evolving conditions. For CLO equity investors, resets offer extended returns and optimised cash flows.

As the CLO market continues to grow, with strong issuance and a robust pipeline of aging CLOs eligible for resets, this area is likely to remain a focal point for investors and portfolio managers. While challenges such as higher-for-longer rates that could impact credit risks warrant attention, the overall outlook for CLO resets is highly promising.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.