A more diverse ILS landscape – but not necessarily more diversified portfolios

The ILS market is expanding. A market that historically covered only natural disasters - such as hurricanes and earthquakes - now offers insurance protection for events such as cyber-crime and terrorism attacks. But while diversification is key to building resilient portfolios, adding some of these new perils to an ILS portfolio might introduce false diversification, as it might actually increase the correlation with wider financial markets.

How ILS work

Insurance companies use ILS to transfer the risk of specific events, often nature-related, to capital markets through financial instruments such as catastrophe bonds (cat bonds). Investors provide capital in exchange for premiums and, if no covered event occurs, they receive their principal back with interest. If a disaster triggers the bond, the insurer uses the funds to cover claims and investors lose some or all of their capital.

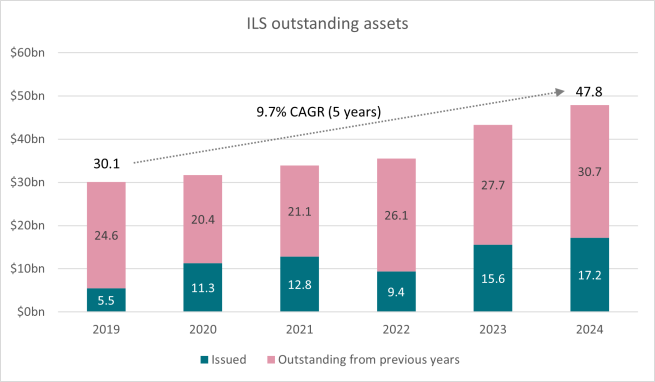

A steadily growing market

2024 was a record year: ILS issuance grew by 10.5% year-on-year and reached $17.2bn. The ILS market is now nearing $50bn of outstanding assets, an annual growth rate of nearly 10% over the past five years.

A more diverse ILS market

As the ILS market grows, it also includes more diverse perils. Coverage of natural catastrophes such as hurricanes, earthquakes and typhoons has expanded to a broader range of risks including wildfire, flood, and severe convective storms. Additionally, newer ILS structures now provide coverage for non-natural catastrophe risks such as cyber-threats, terrorism and even mortality and longevity risks. These are risks related to the financial uncertainty associated with changes in death rates and people’s lifespan, which can impact the payouts of life insurance and pension products.

Cyber attacks

The first cyber-catastrophe bond was issued in 2023, since then the market has seen 10 cyber-ILS issuances totalling over $800m.

Terrorism

The first cat bond focused on terrorism was issued in 2019 in the UK by Pool Re. In December 2024, the first terrorism cat bond outside the UK was issued in France, intended to cover losses from terrorist attacks in France and its overseas territories. These bonds are the first to focus solely on terrorism losses, but there have also been bonds that have had terrorism exposure prior to this – in 2003 bonds were issued to cover a potential cancellation of the 2006 FIFA World Cup, with terrorism stated as the primary risk.

New perils are very different from traditional cat bonds

One thing these two types of perils have in common – and which they don’t share with traditional nature-related cat bonds – is that they are man-made. Because of this there are ways for insurers to mitigate these risks.

In the case of cyber-attacks, insurers can audit and suggest improvements to the policyholder’s computing infrastructure. In the case of terrorism, Pool Re offers a variety of programmes and tools aimed at incentivising good security and risk management behaviours.

Assessing risk

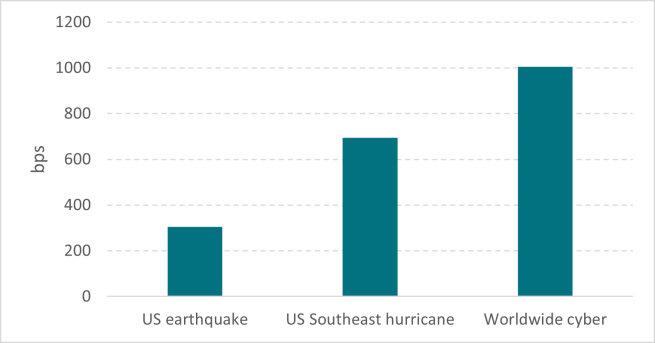

More importantly for ILS investors, these two new perils are more difficult to model the risk for. Unlike natural catastrophe risks, where modelling frameworks have been refined over decades and where for example seasonal and geographical patterns impact the risk assessment, cyber risk is less understood and keeps evolving.

This means that exposure limits are also more difficult to estimate, and consequently pricing these risks becomes more complex. This is one of the contributing factors to the relatively high coupon rates on cyber-bonds.

Correlation with wider financial markets

Another important factor is that some of these new perils might be more correlated with financial markets than traditional cat bonds, which have had virtually no correlation with economic cycles. A large terrorist attack is likely to impact financial markets, and a large-scale cyber-attack could impact the share price of entire sectors. This means that investors who are trying to build more diverse and resilient portfolios could, in reality, end up with portfolios that are less diversified as part of a wider alternative credit allocation.

A different approach

Adding new perils to ILS portfolios could enhance its diversification – a key factor in most portfolios, but it does not necessarily improve the diversification for the end investor, as new perils are at risk of higher correlation to markets and more complex/less accurate modelling. For this reason, we tend to favour geographic diversification over adding new perils.

We have been investing in ILS since 2007 with a track record through various natural catastrophe events. We have a dedicated investment team with an expertise in risk projections. To add new perils, we need to have a certain level of conviction that we can accurately assess the level of risk and they need to adhere to our very strict risk assessment tools. We believe the potential additional return these new perils can offer might not always be worth the additional – and often complex-to-assess - risk.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.