Alternative credit outlook: Risk appetite is back, but performance won’t be evenly distributed

Key takeaways

- Market sentiment has grown cautiously optimistic, but rates will stay higher for longer.

- Value corrections have created attractive entry points in real asset sectors, supported by significant financing needs.

- Geopolitical events will impact risk appetite, but structural trends and bank disintermediation continue to create opportunities.

Risk assets have had a strong first half of the year. While rates have remained higher than expected due to stubborn inflation, corporate profits have been resilient thanks to surprisingly solid consumer spending. Markets now expect a soft landing for the US economy, and this cautious optimism should continue to drive a risk asset rally in the second half of 2024.

Three main themes will drive Alternative Credit performance over the next six months.

1) Global rates to remain higher for longer

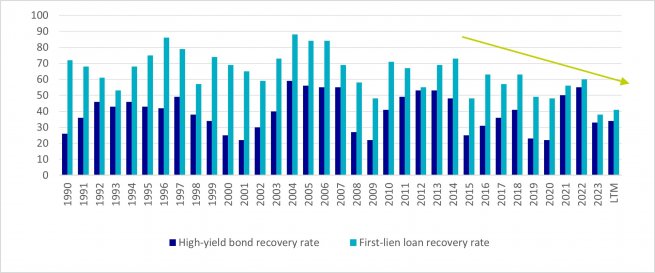

While major central banks are still in the process of balance sheet reduction, markets no longer expect rates to be cut as rapidly as they thought a year ago. Compared to previous periods of rate hikes corporates have been highly resilient, with global corporate defaults remaining below their historical average. However, high financing costs for a prolonged period will negatively impact businesses and households. Loan recovery rates are trending downward (see chart below), reflecting more covenant-lite structures over the past few years. At the same time, increasing financing costs are now also eroding companies’ cash flows and coverage ratios, leaving them more vulnerable to external shocks and interest rate uncertainty.

In this environment fundamental credit selection and sector differentiation will remain important.

Attractive entry points but uneven recovery

Within real estate lending, higher borrowing costs have put pressure on yields for prime assets. The recovery in valuations that we have started to see won’t be evenly distributed. It will instead be based on location, structural trends supporting specific sectors, and energy efficiency.

Valuations will also be supported by a pent-up demand for financing. Sponsors held off refinancing during the recent hiking cycle. But structural trends such as digitalisation and decarbonisation have increased the investment needs in many real asset sectors. Liquidity will be in demand over the next few years and this puts alternative lenders in a good position to negotiate attractive covenants.

With rates having peaked, we see this as an opportunity to lend at lower loan-to-value ratios (LTVs) and on rebased valuations. But the factors mentioned above are absolutely essential.

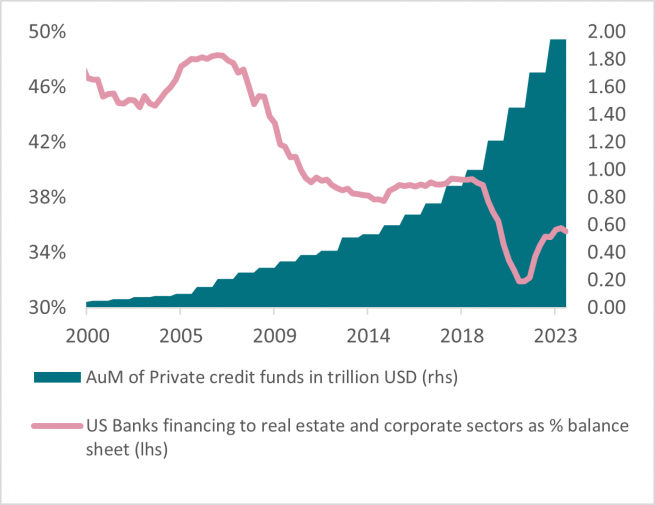

2) Private market lending benefitting from bank disintermediation trend

Higher-for-longer rates have exacerbated the ongoing trend of banks retreating from certain lending activities. Lending surveys still show that banks are not willing to ease lending standards, resulting in restrained capital flows to the economy. Private credit will continue to fill this funding gap.

With less competition from banks, alternative lenders can achieve better spreads and more lender-friendly structures. Examples are more conservative LTVs, tighter covenants and prepayment penalties.

3) Markets remain vulnerable to adverse shocks

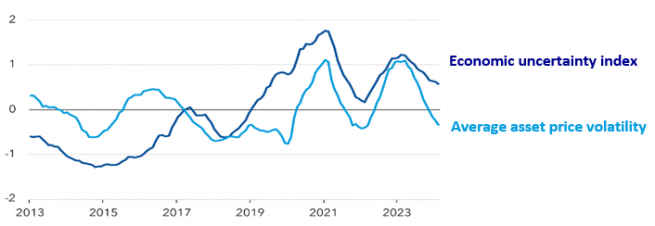

The market rally has led credit spreads to narrow, and risk premiums have compressed. But while inflation has started to fall, high rates have left corporates more sensitive to geopolitical risks which could lead to macro shocks.

Over the past 12 months, asset price volatility has trended lower than measures of economic policy uncertainty. This difference highlights the risk of rapid rebounds in volatility, leaving markets vulnerable to repricing risks.

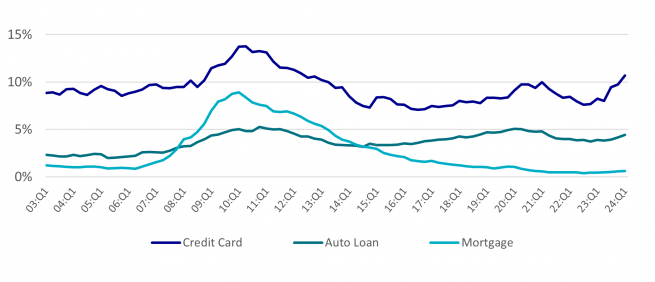

Deteriorating consumer data

This elevated economic uncertainty, and higher-for-longer rates, have also started impacting consumption. Better-than-expected economic growth and a strong labour market have been the main drivers of performance for consumer assets. Prime assets have performed well because of this. But in the weaker parts of the consumer economy, we are starting to see negative delinquency trends.

In the US, more borrowers are falling behind on credit card payments. Delinquencies are also rising on auto loans. With our higher-for-longer scenario in mind, we believe allocation within consumer assets should be tilted to less rate-sensitive assets.

On the more positive side, household debt remains below pandemic levels in many European countries, largely due to wage growth. This should limit the negative impact of higher-for-longer rates and potential adverse shocks.

Attractive opportunities but high dispersion in performance

Higher-for-longer rates and the trend of bank disintermediation will continue to create opportunities for alternative lenders. Better-than-expected economic data should continue to drive the performance of riskier assets as the risk of a hard landing fades. Elevated rates have also created attractive entry points, especially for real asset lenders.

However, high financing costs have left corporates more vulnerable and we are starting to see some negative trends in the more interest rate sensitive parts of the consumer economy. Combined with ongoing geopolitical risks, performance dispersion will be high. Investors will have to be selective and focus on areas that are either supported by structural trends or on parts of the market that are less negatively impacted by higher-for-longer rates.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This text is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this text is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.