Who gets the most impact for their buck?

- Impact investing has grown rapidly over the last decade – but impact investors should be mindful of to what extent tangible impact can really be achieved.

- Unlike with publicly listed companies, Private Equity investors can take a much more active role in their companies.

- By shaping the product and commercial strategy of healthcare companies at the early stage of the product development process, Private Equity healthcare investors can deliver tangible impact in underserved markets.

Impact assets have grown rapidly over the last decade and Impact funds had over $1.5 trillion in AUM in 2024 - an annual growth rate of 21% over the last five years

The growing healthcare Private Equity market

The Private Equity (PE) healthcare market has grown significantly in recent years. In 2024, global healthcare PE deal value reached an estimated $115 billion, the second-highest total on record

The active role of Private Equity investors

PE and listed equity each offer varying degrees of control and influence over the companies they invest in. In public equity, shareholders may exercise voting rights at annual general meetings, but their ability to effect change is often minimal unless they hold a substantial portion of the company's shares. Conversely, PE investors acquire significant – often majority – stakes in privately held companies, granting them substantial control over strategic and operational decisions.

PE investors are able to actively engage in shaping the company's direction – for example through a board seat – and implement value-creation strategies and driving performance improvements.

On the product side, PE investors can deliver impact in two key ways;

- Streamlining operations, renegotiating supplier contracts and implementing leaner manufacturing techniques to reduce costs and improve profit margins - which can help reduce the price point and make the product more accessible.

- Prioritising global mass markets – not just high-income markets – in product development and commercial strategies along with adopting more sustainable practices, enhancing labour conditions and engaging in community initiatives.

Influence on commercial strategy

We see three key ways PE investors can deliver impact through the commercial strategy;

- Centralising procurement processes and leveraging economies of scale, resulting in cost savings and improved supply chain efficiency.

- Expanding the market reach by entering new geographical markets, diversifying the customer base, opening new distribution channels, or pursue strategic partnerships.

- Influencing companies to develop products or services that better address social needs, thereby creating positive societal impact while tapping into new market opportunities.

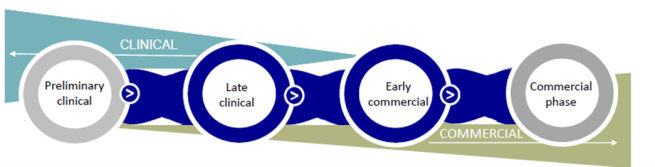

Private Equity investments in healthcare: early-stage vs. late-stage

The healthcare sector is a good example of where PE investors can generate tangible impact, but the level of control and influence on the company depends greatly on what stage the company is in.

Investing in early-clinical stage firms – companies that are at the earliest stage in the drug development process and are testing new drugs to assess their safety and efficacy – allows investors greater influence over strategic decisions including clinical trial designs, regulatory pathways, and initial market strategies. However, these investments carry higher risks due to uncertainties in clinical outcomes, regulatory approvals and market acceptance.

At the other end of the spectrum are late-commercial stage firms. At this stage, companies have established products and revenue streams, resulting in lower-risk profiles. PE investors may have less influence over foundational strategic decisions but can still drive value through operational improvements, market expansion, and optimisation of existing processes.

We consider the late-clinical or early-commercial phase to be ideal, as we can deliver significant change while excluding the riskiest phase. These companies have clinical data that has proven the efficacy of the product, but they are still early enough in the process to allow a PE investor influence on the market and product strategy.

How this works in reality - Alydia

AXA IM Alts, through its healthcare strategy, invested in Alydia Health in 2020. At the time, Alydia was completing a pivotal study for a device to evaluate its ability to treat postpartum haemorrhage (PPH).

According to the WHO, up to 14 million women experience PPH each year resulting in 70,000 deaths. The most common cause of PPH is uterine atony, which is the inability to contract after labour. Alydia’s Jada Device facilitates uterine contraction and is simple to use for healthcare workers. The pivotal study showed 94% efficacy, with most women’s blood loss ceasing in under five minutes. This impressive data led to US Food and Drug Administration (FDA) clearance.

We were both members of the Alydia board of directors and we worked with the company to increase study enrolment, hire a commercial CEO upon FDA clearance, and drive an exit process. Alydia was acquired by Organon (a women’s health company which was a spinout from Merck) in 2021.

The Jada device is now in approximately 90% of high-volume labour and delivery hospitals in the US. Organon recently received European approval and will begin commercial work there this year. Zina Affas Besse continues to work with Organon as part of the Global Access Committee, leading efforts to introduce Jada into low- and middle-income countries.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.