Asset Backed Securities : Resilience in uncertain times

Key takeaways :

- Slowing growth, higher-for-longer rates and volatile markets mean investors have to look further to find yield without excessive risk.

- ABS have proven their resilience in previous periods of market stress. They also tend to offer investors higher spreads compared to fixed income assets with similar ratings.

- Today ABS gives investors a unique access to consumer assets, important diversification benefits and attractive spreads in a highly liquid market.

How can the higher rate environment, which is squeezing borrowers, create opportunities in Asset Backed Securities (ABS)? The ABS market has undergone significant changes over the last decade, especially from a regulatory perspective, and today offer investors very attractive yields and highly defensive performance in times of volatility. Given the current market environment, we believe this could be a great time to add ABS to an institutional portfolio.

Economic headwinds and volatility require resilient portfolios

Interest rate uncertainty accompanied by slowing global economic growth means investors have had to look closer at where they can find the defensive exposure they expect from bonds, while still getting sufficient yield. This has become even more important as inflation remains high, and investors need to make up the shortfall between cash rates and inflation.

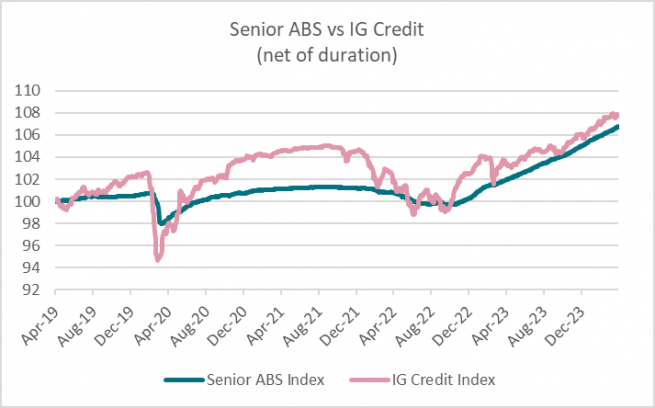

The high level of rates is now also starting to take a toll on consumer spending, which will likely lead to a slowdown in growth. Over the last few years ABS have been highly resilient and offered less volatility than IG credit.

We recently highlighted in our Alternative credit outlook why we believe the heightened level of market volatility will be around for some time. We also expect rates to stay higher for longer and geopolitical risks to remain. In this environment ABS can offer investors more protective features.

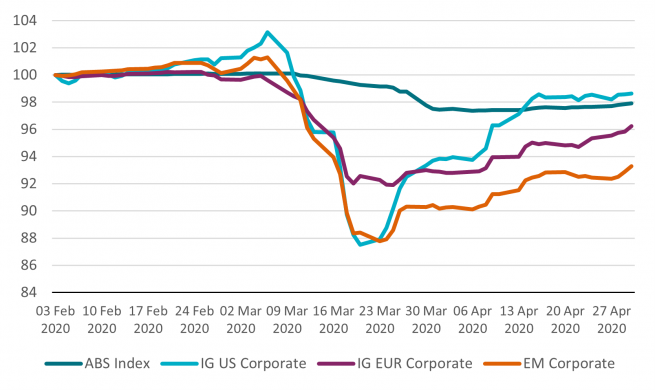

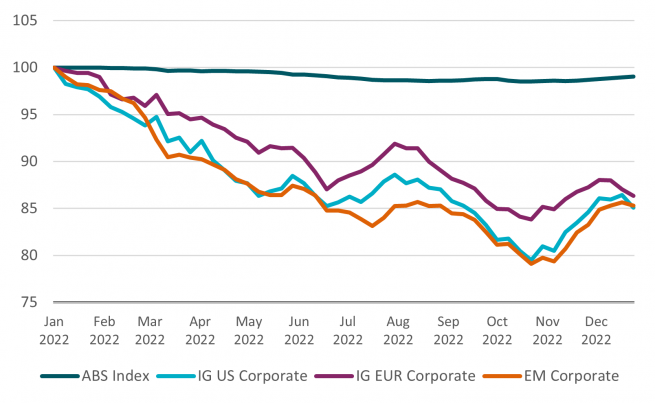

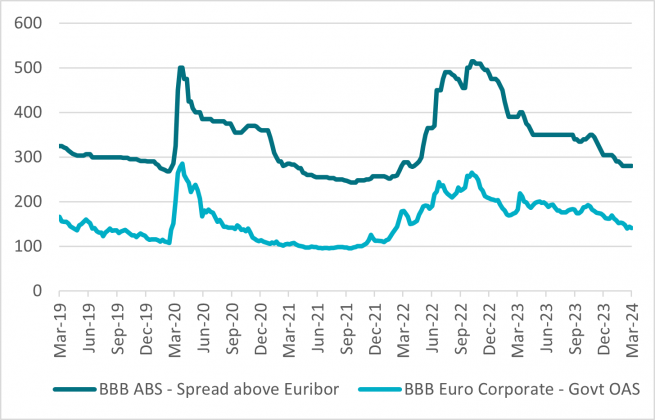

For example, the ABS market proved extremely resilient throughout the onset of the Covid pandemic and during the heightened market volatility in Q4 2022 (figures below). This downside protection is largely due to the backing of high-quality, defensive collateral.

Investor-friendly features and regulatory changes

There are a few key reasons behind these characteristics. ABS are floating rate notes, and therefore have very low duration. Secondly, ABS are in general short dated by nature. Thirdly, ABS tranches amortise over time, where principal repayment is made on a regular basis (monthly, quarterly). Amortisation is for example common in ABS/RMBS, but much less common in traditional corporate debt, where the principal payment by the issuers is usually made at maturity. This amortisation reduces the refinancing risks. All these features combined contribute to the very stable performance in times of elevated market stress.

Some of these features are due to a new securities regulation that came into effect in 2019, where a simple, transparent and standardised label was put in place by the EU to establish a capital markets union and to ensure a high degree of protection for investors.

In short, the new rules are much more stringent regarding due diligence, risk retention and transparency for securitised products. This change has led to a more transparent market, as loan-by-loan data from originators is now mandatory and it has also resulted in more favourable Solvency II treatment across the ABS capital structure.

Yield without moving down the quality scale

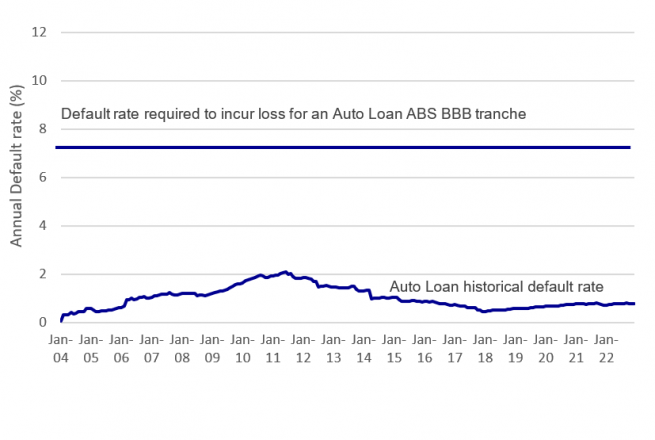

While the high interest rate environment continues to weigh on corporates and consumers, ABS have performed relatively well as underlying factors remain positive: consumer assets are supported by low unemployment rates and corporates have been in a benign default environment.

High interest rates also bring about positive aspects from a yield perspective. The floating rate nature of ABS instruments ensure that all-in-yields are – and if our view on rates is correct – will continue to be highly attractive, especially on a risk adjusted basis. As can be seen in the table below, Investment Grade ABS assets tend to offer higher yields than traditional Investment Grade fixed income assets.

Diversification in a choppy market

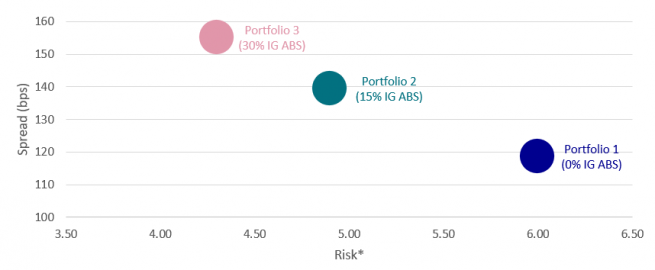

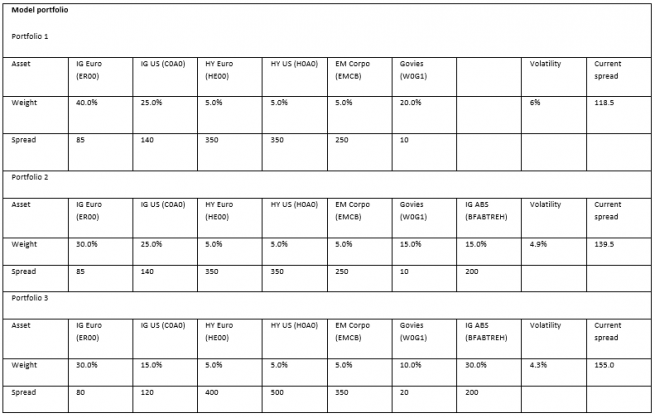

Given the macro headwinds we have already mentioned, we believe diversification will play a key role in portfolio performance this year. The ABS market covers both consumer, corporate and real assets and it is therefore a useful diversifier.

To give an example of this, we have looked at 10-year historical volatility and through a simulation shown that by adding ABS to a typical fixed income portfolio (comprised of global government bonds, euro/US corporate IG credit, euro/US HY credit and some Emerging Market (EM) corporate debt) the level of volatility can be drastically reduced. And as the chart shows, by adding ABS to a portfolio, the lower volatility would contrary to what could be expected not result in a lower, but a higher spread.

An asset class backed by the real economy

Today, the ABS market is supported by a well-established investor base across money managers, bank treasurers, insurance companies, pension funds and other investors looking for high-quality, investment grade alternative fixed income investments. It offers investors a unique access to consumer assets, as well as to corporates and real assets. Due to the breadth and depth of economic activity that ABS supports, opportunities to gain selective exposure to specific areas of the consumer economy are vast.

ABS have proven their resilience during previous bouts of market stress, partly due to the improved liquidity because of significant regulatory changes. Despite this, the asset frequently offers wider credit spreads than comparable lower-rated IG credit – which unlike ABS, is a largely unsecured asset class. With higher-for-longer rates, we believe the ABS market is a great source of value in liquid credit markets today. ABS offer high credit ratings, security against tangible assets (such as property) and robust structural safeguards to maximise the probability of repayment.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This text is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this text is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.