Asset-Based Finance – too important to ignore

Key takeaways

- The Asset-Backed Finance (ABF) universe is rapidly growing and significantly larger than the direct lending market.

- ABF provides investors with access to a wide variety of exposures, typically with shorter duration and higher control than traditional lending.

- By adding ABF to a traditional investment grade or high yield fixed income portfolio, investors can improve the return potential without adding additional risk.

An asset class too big to disregard, supported by banks’ retrenchment

Many investors and asset allocators think primarily of Direct Lending when discussing private credit. Yet this belies an increasing focus on Asset-Based Financing (ABF), a market which has grown exponentially over the last 20 years. Despite this increased awareness, we believe allocations to ABF are still below their optimal levels and that investors are yet to harness the diversification potential of an asset class which permeates every aspect of our lives.

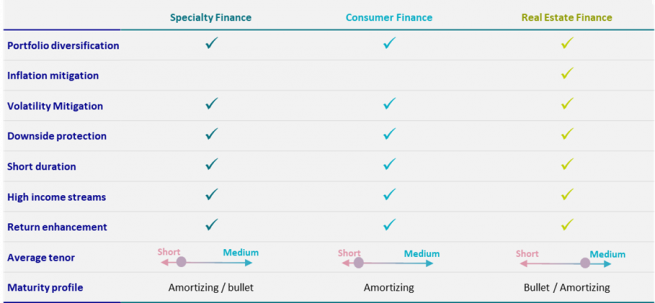

The reasons for ABF's attractiveness are manifold. Compared to direct lending, ABF is highly diverse and gives investors access to the full private credit market including residential mortgages, consumer debt, commercial real estate loan, specialty finance and infrastructure debt. Furthermore, ABF provides exposure to multiple geographies, reducing country-specific risk.

ABF has come to play a more important role in the lending landscape due to the funding gap caused by banks’ tightening lending standards and withdrawal from certain lending activities. ABF is not competing with banks. Instead it is complementary. In many areas, we co-originate deals. We also provide banks with liquidity in secondary markets and, in some areas of ABF, we provide banks with capital relief.

What role can ABF play in a portfolio?

In an environment characterised by interest rate uncertainty, higher-than-average market volatility from geopolitical risks and rising corporate defaults, ABF offer investors important benefits that traditional credit doesn’t.

- Backed by assets: An important share of ABF is backed by physical or financial assets, thereby facilitating the recovery of principal in the event of default. This offers a certain level of protection and resilience in times of economic weakness. A majority is also fully amortising, further reducing downside risk.

- Typically short duration: As ABF differs greatly in duration, it is a way to limit exposure to interest rate risk.

- Income premium: Due to complexity and illiquidity premiums, as well as a more limited investor base, ABF generally offers an income premium compared to traditional fixed income products.

- Greater control: This can range from covenants to, for example, a large investor arranging a bilateral relationship with the borrower which generally results in better alignment of interests and more investor-friendly features.

Portfolio optimisation through high diversification

ABF can act as an effective diversifier in a traditional fixed income portfolio. In addition to low correlations with publicly traded fixed income, it also has low intra-asset class correlations.

Incorporating ABF into a traditional IG fixed income portfolio

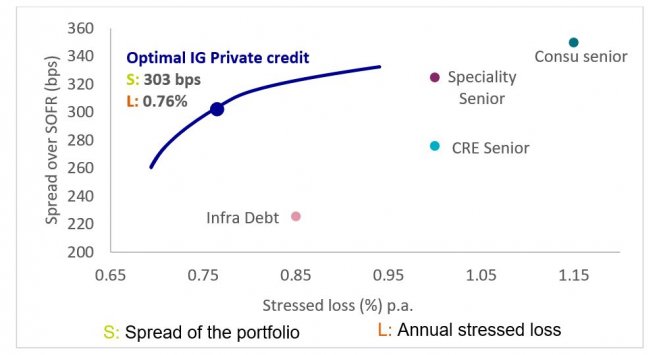

To illustrate the diversification benefits of ABF, we have estimated loss levels and spreads for some of the larger ABF asset classes. We have defined annual stressed losses throughout an entire credit cycle as an appropriate indicator to measure risk. This gives a more accurate picture as volatility in private markets is often difficult to correctly estimate due to the lower trading frequency.

By plotting the risk and return profiles of selected ABF asset classes, we can show how the efficient frontier of a traditional IG credit portfolio - the optimal combination of assets with the highest risk-adjusted return for each level of stressed losses - achieves significantly improved spreads when combined in a diversified portfolio than those achieved on the individual asset classes.

Increased return potential without added risk

In our example, we achieve the optimal risk-adjusted return by replacing 20% of a traditional IG debt portfolio with IG ABF. By adding this optimised blend of ABF asset classes, we achieve better diversification. But more importantly, expected return (‘blended portfolio’, below) rises by over a third with minimal changes to the estimated annual stressed loss of the portfolio.

This example is even more striking when applied to a 'traditional’ high yield debt portfolio. In our analysis, the expected carry of a traditional HY credit portfolio increases by 26% and the annual stressed loss is expected to reduce by 11%.

Optimal ABF allocation in a traditional HY debt portfolio

The investment opportunity

The disintermediation of traditional bank financing continues to benefit ABF. Tighter lending rules and higher interest rates further boost this growth. Technological advances will also have an impact. To give an example, non-bank mortgage lending has risen rapidly in the US due to the rise of online lenders. A similar trend is seen in Europe.

But investors should keep two factors in mind. Unlike publicly traded debt, ABF always requires a bottom-up approach with a detailed knowledge of sectors and issuers. Expertise and access to data, partly gained through a long track record, is essential in this highly diverse market. And size matters. Large investors can source deals that smaller players might not be able to. Size also allows having more established relationships with a larger number of issuers.

ABF offer investors an opportunity to finance the real economy and benefit from diversification and yield enhancement. As more lenders and borrowers discover these attractive opportunities, allocations keep increasing and the asset class is growing both in size and number of sub-asset classes. ABF is likely to follow the same rapid expansion as direct lending has over the past decade, and become too big for investors to ignore.

Source

*Consumer finance – mezzanine (AXA IM proxy), CRE Debt – Enhanced (HURE index), Infrastructure debt (Markit iBoxx EUR Infrastructure Index), Direct Lending (Cliffwater Direct Lending Index), Specialty finance Mezzanine (AXA IM proxy), US HY credit (BofA H0A0 Index), US IG credit (C0A0 Index).

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.