Investment grade ABS - Liquidity and spread pick-up in times of turbulent markets

Investment grade ABS - Liquidity and spread pick-up in times of turbulent markets

- With ongoing geopolitical risks, interest rate uncertainty, and slowing growth, investors might want to widen their investment universe to find high-quality, liquid options that can deliver attractive spreads without adding significant risk.

- Investment grade (IG) Asset-Backed Securities (ABS) provide resilient characteristics, particularly during periods of market stress, as well as spread pick-up compared to similarly rated corporate debt.

- The asset class has proven to be highly liquid, even during previous periods of elevated market volatility.

Volatile markets. Slowing global economic growth. Fears that some central banks have kept rates too high for too long. These factors mean investors need to review their allocations to avoid being left with portfolios that aren’t defensive enough, while still achieving sufficient yield. In this environment, investment grade ABS offer very attractive return and diversification benefits, while allowing more flexibility than many other areas of the private credit market.

What are ABS?

ABS are instruments backed by pools of assets such as loans, leases, or receivables, where the underlying assets are bundled and then sold as tranches with varying risk levels. Investors receive payments from the underlying assets' cash flows, such as mortgage payments or auto loans. ABS have existed for over 20 years and provide finance to consumers, and to a lesser extent corporations and the real estate sector. They bring diversification and protective features to investors, some of which we’ll explore here.

Spread pick-up compared to traditional investment grade credit

Investment grade ABS tend to offer higher yields than similarly rated traditional investment grade fixed-income assets, as shown in the table below. From a yield perspective, high interest rates have positive aspects, as the floating rate nature of ABS instruments ensures that all-in yields are attractive, especially on a risk-adjusted basis. This yield pick-up is partly due to ABS being more complex instruments and they are also not available to all investors, leading to a reduced client pool.

Spread pick-up without additional risk

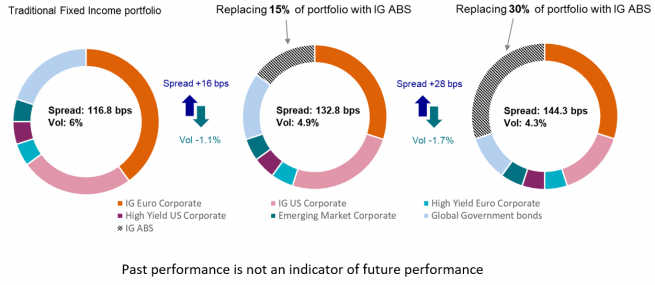

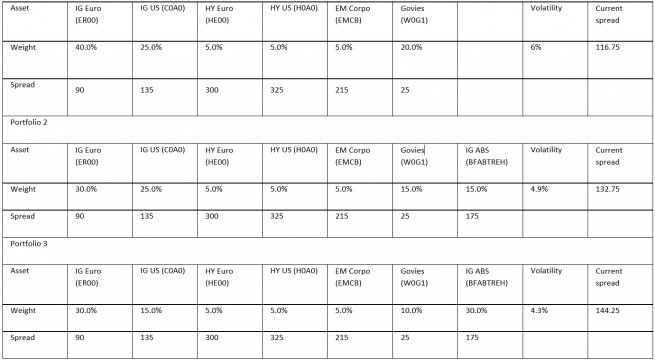

To illustrate how institutional investors can benefit from this spread pick-up and create more resilient portfolios, we have created a historical example to show how adding ABS to a portfolio could enhanced returns. We examined 10-year historical volatility and found that by adding ABS to a typical fixed-income portfolio (comprising a blend of government bonds, IG credit, high-yield credit, and Emerging Market corporate debt, see table at end of article), the spread can be improved without increasing the level of volatility.

In fact, due to the significant diversification benefits of ABS, the volatility of the resulting portfolios is lower than that of the traditional fixed-income portfolio. For the right chart – in which we increased the IG ABS allocation to 30% – the spread increased from 117 to 144 basis points, while the volatility decreased from 6% to 4.3%.

Resilience across economic cycles

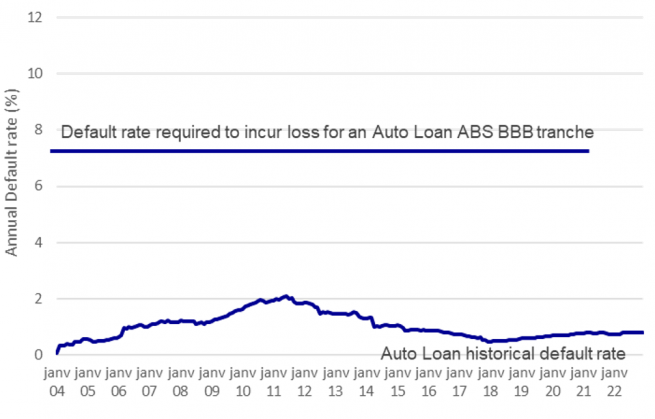

So what is it about ABS that allow them to provide higher all-in yields for lower risk? Due to the structure of ABS, they have performed well during previous periods of market stress. For example, auto loan default rates would need to rise significantly above their long-term averages—and much higher than they did during the Global Financial Crisis (GFC)—to impact BBB-rated auto loan ABS. In addition, consumer data has remained strong with low unemployment rates, resilient spending and savings rates, all of which are important factors for ABS. Simply put, the additional spread pick-up is not largely due to additional risk but to a few specific other factors.

One of the factors is the fact that ABS are collateralised, which contributes to their robustness during periods of elevated market volatility. Other factors include:

- ABS are floating rate notes, and therefore have very low rate duration.

- ABS are generally short-dated, given the nature of the underlying loans (consumer loans, auto loans).

- ABS tranches amortise over time, with principal repayments made regularly (monthly or quarterly). Amortisation is common in ABS/RMBS but much less common in traditional corporate debt, where principal repayment by issuers is usually made at maturity. This amortization reduces refinancing risks.

Liquidity without losing access to alternative credit features

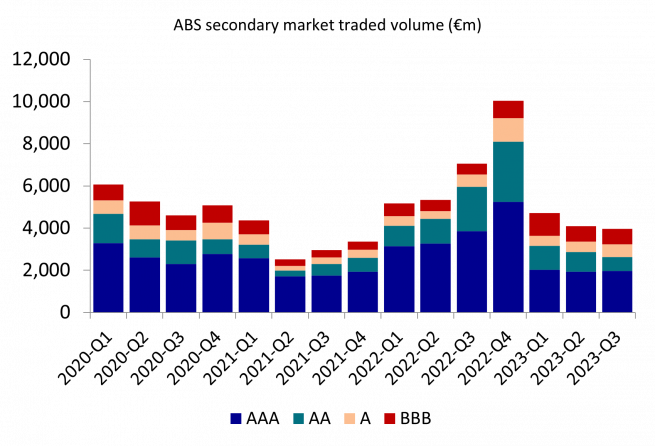

Many investors would agree that the spread and volatility figures shown above are very compelling, but some might still question the quality and transparency of the ABS market, as well as its liquidity. After all, loans are bundled together and sold as separate assets, so investors are right to want to know about the underlying assets.

Over the last decade, key regulatory changes aimed at making the ABS market more transparent and less risky have led to growth in both issuers and investors. This has also resulted in significantly improved liquidity and transparency in the market. For example, in Europe, uniform standards for transparency, risk retention and due diligence have been implemented across the EU.

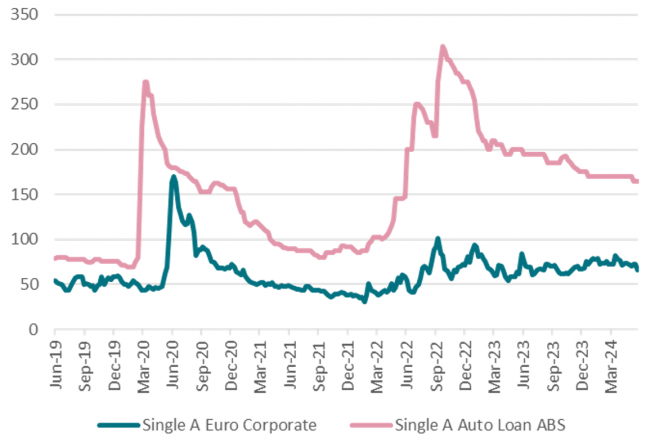

The improved liquidity can be seen during recent periods of market stress, such as early 2020 at the onset of COVID-19 and in October 2022 during the UK mini-budget sell-off, with ample liquidity in the market. This is an important factor for investors worried about current macro headwinds, as liquid strategies allow for a more flexible and dynamic allocations.

A liquid asset class that should be a staple in fixed income portfolios

Today, the ABS market is no longer niche but highly diverse and transparent, frequently offering investors wider credit spreads than comparable investment grade credit—which, unlike ABS, is a largely unsecured asset class. It also offers important diversification benefits, the significance of which cannot be overstated in the current market environment. By adding ABS to a traditional fixed-income portfolio, we have shown that investors can achieve higher spreads and lower volatility without sacrificing liquidity. This should put liquid ABS top of investors’ minds.

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.