Decarbonisation is the number one challenge for the real estate industry

- The real estate sector accounts for about 39% of global greenhouse gas emissions and much more needs to be done to decarbonise.

- Our Green Shift project aims to decarbonise our existing as well as new real estate developments by aligning our assets’ emissions with defined pathways.

- We start with the most cost-efficient measures and then prioritise assets likely to derive enhanced returns from capital expenditure.

Global emissions require urgent action

Climate change has led the real estate industry to a pivotal point. Regulatory pressure to bring the industry in line with climate targets has increased, particularly in Europe. Investors have made Net Zero commitment, putting increased pressure on asset managers to be deliberate and transparent about their decarbonisation plans. And tenants are demanding more sustainable buildings – either as part of corporate commitments for business occupants or through social and political pressure in the residential space.

It is a huge challenge for a sector that accounts for approximately 39% of global greenhouse gas emissions1 - both from operating buildings and from constructing or refurbishing them. The stark reality is that approximately three quarters of standing assets today are carbon inefficient2. And there is not enough development to meet the increasing demand for green-certified buildings, which could lead to a 70% shortfall in available low-carbon buildings as soon as 20303. Yet despite the sector’s crucial role in the climate transition, there has been a lack of tangible action from the industry to date.

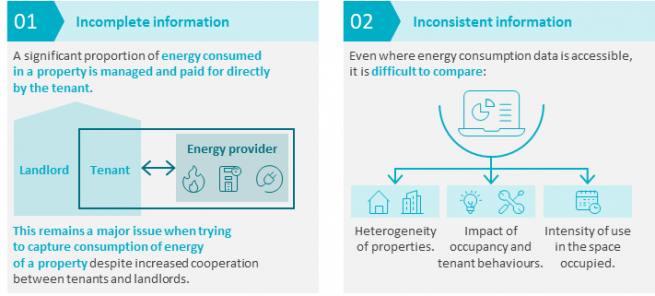

Data availability and comparability are major hurdles

One of the key challenges is data. It can be difficult to understand the energy performance of each individual asset, particularly as tenants typically make their own arrangements for energy consumption. This leaves landlords to either approximate the energy use of a building or to engage with tenants to procure ‘actual use’ data.

A second problem is the non-heterogeneity of buildings. A supermarket needs to keep many items chilled; a warehouse may need 24hr lighting; the demands on an office building can vary drastically depending on the day of the week. And even in the same type of building, tenant requirements and behaviours can vary significantly.

Running out of time to act

But imperfect data cannot be a reason for lack of progress, especially when the need is so pressing. To be clear, this need is not ideological. Real estate investment managers have a fiduciary duty to sustain and enhance both the liquidity and the performance of investors’ portfolios. In simple terms, there is a carrot and a stick. The carrot is the increasingly observable ‘green premium’ for low-carbon buildings. The stick is a drift towards obsolescence, otherwise known as stranded assets.

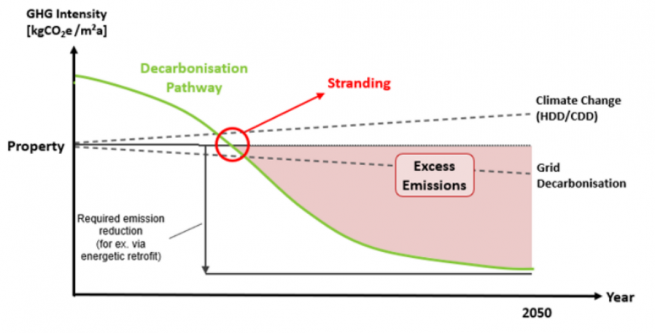

A pathway, not a switch

Through the advent of tools such as Carbon Risk Real Estate Monitor (CRREM), asset managers are better able to calculate the stranding risk of buildings by country and by sector – plus the path they should take to obviate this risk. The pathways measure greenhouse gas emissions (GHG) and are aligned with limiting global warming to 1.5°C and 2°C by 2050.

However, the size, scope and expense of real estate projects mean that planning to meet this target must happen many years before the target date. It needs to start now.

Introducing Green Shift

Our Green Shift project has been two years in the making. It has involved a huge commitment in terms of team resource, training, data consolidation and investment in tools. Through this methodology, we embed decarbonisation into all aspects of our real estate activities.

This commitment allows us to analyse each and every one of the standing assets we manage for investors. Through detailed energy data and a consistent, comparable understanding of each property’s energy and carbon performance we are able to prioritise those assets with the greatest potential to derive additional value and returns.

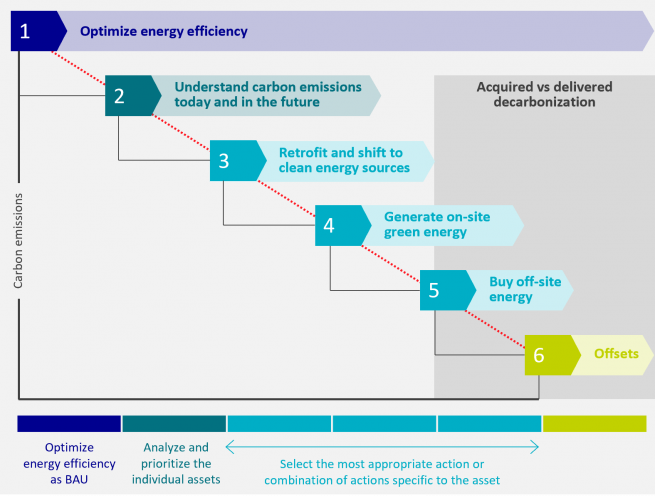

Standing assets – a constant focus on cost-effective measures

We start by focusing on the most cost-effective measures, with an ongoing emphasis on activities that will improve energy efficiency. There may motion sensors to manage lighting or better building management. An important part of this is engaging with our tenants, making sure they are aligned with our objectives. The same applies to our property managers. For example, we establish property manager agreements that focus on energy performance and monitoring – with defined reporting, KPIs and incentives.

Beyond the ongoing optimisation of energy efficiency, many buildings will require a cost-benefit analysis to decide whether and to what extent capex should be deployed. This capex can vary widely. There may be changes to façades, windows and insulation that significantly lower emissions. It could be that there’s a way to efficiently change the main energy source or even install, for example, solar panels.

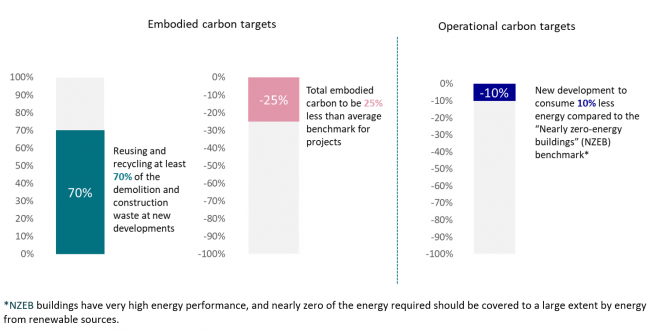

Development – delivering assets for a Net Zero future

For development, there is more scope to influence a building’s energy and carbon profile through life-cycle analysis and with a particular emphasis on the planning stage. That is why we have ambitious, clearly defined targets for both embodied and operational carbon for our new developments.

Next steps

Climate change is an urgent challenge. Regulatory requirements and evolving tenant demands make this especially urgent for real estate, which must adapt or see assets become obsolete. This decarbonisation project is one of our key priorities over the next few years and we are allocating significant resources to reach our ambitious targets. We have 12 ESG experts and over 130 asset managers globally who will implement our plan and work hard to make sure all our tenants understand the challenge and contribute to the success of this project.

We continue to survey our existing assets, prioritising assets which will be most enhanced by bringing them in line with the CRREM pathway. We strongly believe that this project can be positive from a sustainability perspective and via the potential for enhanced returns from improving the assets we manage on behalf of our clients.

1 Source: McKinsey as of July 2023.

2 Source: JLL Research, 2023. The green tipping point: Is 2024 the year when carbon commitments change lease markets at scale? 75% inefficient stock refers to current European building stock which is carbon/energy inefficient.

3 Source: JLL Research, 2023. The green tipping point: Is 2024 the year when carbon commitments change lease markets at scale? 70% unmet demand is the estimated global shortfall of supply by 2030, given the current quality of existing stock and development pipeline.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.