Selectivity - and size - matter in a growing ILS market

- The Insurance-Linked Securities (ILS) market continues to grow, not only in size but also in types of perils covered, as insurers increasingly turn to capital markets.

- A larger and more diversified ILS market means investors can be more selective.

- Smaller investors can be even more nimble and invest only where they have the greatest conviction.

Climate change and increased need for diversification is fuelling issuance

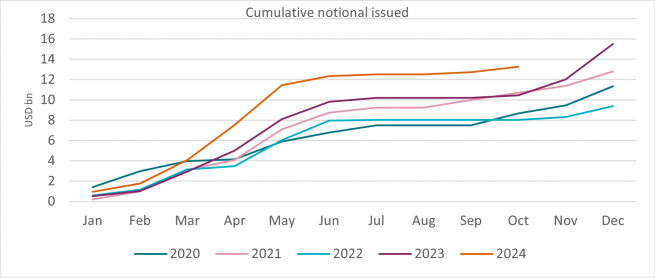

The Insurance-Linked Securities (ILS) market is booming. The first half of 2024 saw record issuance in the primary market, continuing the trend from 2023 when total issued capital surpassed $100bn for the first time. In H1 2024, there was over $12.3bn of primary issuance[1].

How ILS work

Both demand and supply factors have contributed to this growth. On the one hand, investors are increasingly attracted to ILS’s uncorrelated returns, especially during times of interest rate and spread uncertainty. On the supply side, issuers are seeking alternative ways to transfer insurance risk, which is increasingly important considering a growing population, a rising number of natural disasters and the impact of climate change.

Insurance companies use ILS to transfer the risk of specific events, often nature-related, to capital markets. ILS co-exist with reinsurance markets and are complementary rather than competing. Key differences include that insurers use ILS to access a broader pool of capital, often at a higher cost than traditional reinsurance, and different tenures – reinsurance contracts typically cover one year, while ILS is spread over a longer period, often around three years. A large part of the ILS market is made up of catastrophe bonds (Cat bonds), which mainly cover natural disasters.

A bigger market means better opportunities to be selective

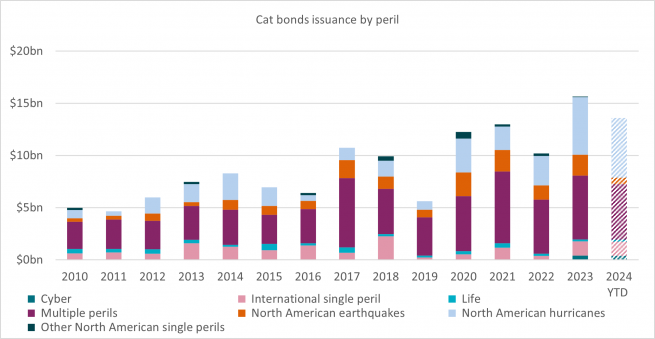

In addition to growing in size, the breadth of covered perils is increasing, with significant growth of non-natural catastrophe risks. Over the past few years ILS have, for example, been issued to cover cyber risks. The cyber (re)insurance market is still relatively small, worth around $17bn in 2023, but is expected to grow at an annual rate of around 26% until 2030[2]. ILS issuance is also covering risks that are more widespread geographically. For example, in 2023 ILS was issued to cover German earthquakes, the first time this specific peril and country was covered.

Because of this, ILS portfolios are in general becoming more diversified, both from a peril and a geographic perspective. Crucially, this means that ILS managers can be more selective. The ILS market has more than doubled in size since 2013. As the market grows, ILS managers are better able to invest only in areas where they can relatively accurately assess the level of risk and where they have a solid conviction.

Liquidity is improving

Another positive implication of the growing market is that the secondary market is becoming more liquid. In 2023, there were record trading volumes on the secondary market. This allows ILS managers to be more dynamic in their allocations and it also provides better liquidity on a portfolio level.

Bigger is not always better

However, while the size of the market is clearly positive from a selectivity, diversification and liquidity standpoint, the same rule doesn’t necessarily apply when it comes to the size of the portfolio manager. The ILS market is highly complex, and ILS managers need a deep understanding of nature-related risks and their economic impact. Experience and expertise are important factors when choosing an ILS manager, but so is size. A smaller portfolio manager can, by definition, be more selective when allocating capital.

While the ILS market is growing, it is nowhere near the size of other more mature alternative credit asset classes. This means that large ILS portfolio managers might at times be forced to deploy capital in less attractive parts of the market. A smaller portfolio manager is – simply put – less likely to have to lower their standards when screening issuers and perils. Compared to some other, slightly larger ILS investment managers, we are more likely to be able to exclude perils and issuers that do not fit our risk/return criteria.

Unique diversifying benefits and boosted by structural trends

ILS is a steadily growing asset class with unique diversification benefits and attractive returns. With its floating rate structure, the market has also benefited from its resilience to interest rate changes.

In a previous insight we detailed how inflation has been a factor for ILS returns, significantly impacting the cost of repairs and replacements. Inflation now appears to be under control across most of the globe, which should continue to benefit the asset class.

But it’s important to keep in mind that selectivity is key in this technically complex market, and that being smaller can often allow managers to be more selective. In a market where risks are impacted by climate change and in which new and more diverse perils are covered each year, selectivity will be the main driver of performance.

Disclaimer

Not for Retail distribution: This marketing communication is intended exclusively for Professional, Institutional or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued by AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.