Rising rates create attractive opportunities in Leveraged Loans for active investors

The rising rate environment of the past 18 months has led to numerous benefits for active managers in the Leveraged Loans market, and we believe it’s currently offering investors a highly attractive entry point. Global loans are currently paying SOFR/EURIBOR plus more than 5%[1], well above historical averages, while also giving investors access to highly diversified and liquid portfolios. However, fundamental credit selection, diversification and active trading are essential to mitigate the tail risk from global economic uncertainty and challenges to corporate creditworthiness.

Leveraged Loans are sub-investment grade, high spread, floating rate instruments that are used for a variety of different corporate financing purposes. They sit at the most senior part of the capital structure and are secured against the assets and cash flows of the borrower.

Impact of rising rates

Inflation has led to the rapid rise of interest rates and this has impacted the Leveraged Loans asset class in different ways. On the one hand, rising rates benefit investors, since loans pay interest based on a floating benchmark (SOFR/EURIBOR) and a spread. This floating benchmark resets higher as rates increase.. Compared to high yield bonds, where interest payments are based on fixed rates, Leveraged Loans have proven their resilience in a rising rate environment.

Additionally, in the current period of broad inflation, corporates are more easily able to increase selling prices in order to maintain profitability and cash flow. Broad inflation also continues to facilitate debt erosion.

On the other hand, however, higher interest rates have increased debt service costs and put pressure on corporate cash flows and liquidity positions - all else being equal, this increases the probability of default.

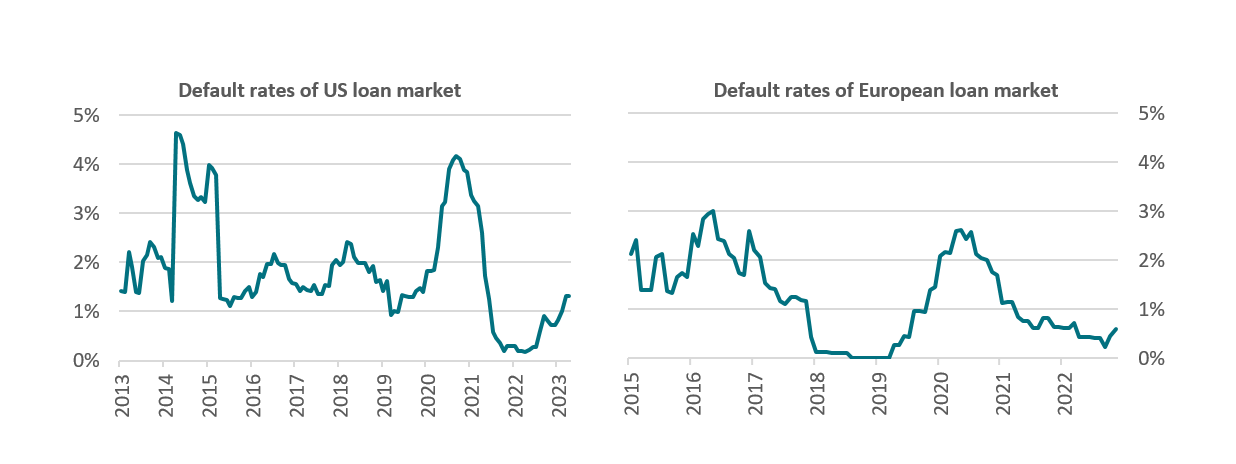

An asset class with a resilient track-record

It should nevertheless be noted that default rates are still relatively low and while they are likely to rise, we do not expect them to move significantly above historical averages for a few reasons:

-

Corporates entered the current economic downturn with strong liquidity positions.

-

Many corporates have been proactive in managing increased interest rates by using interest rate hedges to limit the negative impact on cash flows.

-

Many companies have successfully mitigated the refinancing risk. The maturity wall of the market is now back-ended and does not peak until a few years from now (2028/2029), meaning companies generally do not need to access capital markets in the short term.

-

GDP growth has proven resilient so far despite rapidly rising interest rates.

Leveraged loans are also protected by their senior secured position in the capital structure. In the case of default, we expect recovery rates of 50% - 60%[2] over the cycle.

[1] Source: AXA IM Alts as of 30 June 2023.

[2] Source: AXA IM Alts as of 30 June 2023.

Source: Pitchbook (FKA S&P) LCD Index Page– Morningstar LSTA LLI Maturity Breakdown, April 2023. AXA IM, JPM. Morningstar LSTA US Leveraged Loan Index (LLI). Morningstar European LL Index. For illustration only.

Harvesting return and mitigating risk

We believe the best way to deliver returns and mitigate risk in Global loans is through:

- Maintaining a strong fundamental credit selection – in an environment of rising interest rates and potential recession, bottom-up credit fundamental selection is key to mitigating the risk of default.

- Portfolio construction – aiming to create highly diversified portfolios that focus on defensive sectors characterised by stable demand drivers, recurring revenues and high-quality cash flow generation.

- Active management – adoption of an active trading approach for tail risk mitigation, constant re-evaluation of credit quality and strong communication between portfolio managers and analysts to support the active trading, based on a rigorous investment process.

Disclaimer

All data sourced by AXA IM Alts as at June 2023

This message is for distribution to institutional and professional clients only and is not intended for retail customer use. This message is for informational purposes only and does not constitute, an offer to buy or sell, solicitation, recommendation or investment advice. It has been established on the basis of data, projections, forecasts, anticipations and hypotheses which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

The information contained in this message is not based on the particular circumstances of the recipient. This message does not take into account the recipient’s objectives, financial situation or needs.

Furthermore, due to the subjective nature of these analysis and opinions, these data, projections, forecasts, anticipations, hypothesis and/or opinions are not necessary used or followed by AXA IM Alts’ management teams or its affiliates, who may act based on their own opinions and as independent departments within the Company.

This message may also contain historical market data; however, historical market trends are not reliable indicators of future market behaviour.

For illustrative purposes only. There can be no guarantee that any investment strategy described will be implemented or ultimately be successful. All information in this message is established on data made public by official providers of economic and market statistics.

By accepting this message, the recipient agrees that it will use the information only to evaluate its potential interest in the strategies described herein and for no other purpose and will not divulge any such information to any other party.

AXA IM Alts disclaims any and all liability relating to a decision based on or for reliance on this message.

Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM Alts, prohibited.

© 2023 AXA IM Alts and its Affiliated Companies. All rights reserved.

AXA IM and BNPP AM are progressively merging

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.